73 results found | searching for "apac"

-

-

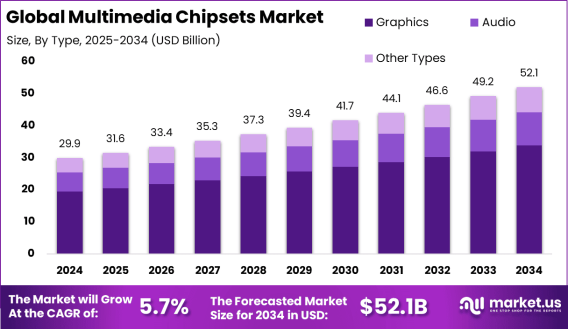

Multimedia Chipsets Market size is expected to be worth around USD 52.1 Billion The Global Multimedia Chipsets Market size is expected to be worth around USD 52.1 Billion By 2034, from USD 29.9 billion in 2024, growing at a CAGR of 5.7% during the forecast period from 2025 to 2034. In 2024, APAC held a dominant market position, capturing more than a 43% share, holding USD 12.8 Billion revenue. Read more - https://market.us/report/global-multimedia-chipsets-market/ The Multimedia Chipsets Market is a vibrant industry centered on creating specialized chips that power audio, video, and graphics in devices like smartphones, TVs, and gaming consoles. These chipsets, including GPUs and SoCs, ensure smooth multimedia experiences, from streaming high-definition videos to rendering complex game graphics. They’re critical in consumer electronics, automotive systems, and IoT devices, meeting the rising need for rich digital content. This market thrives on innovation, with companies racing to deliver faster, more efficient chips for an increasingly connected world. The Multimedia Chipsets Market, as a market landscape, is growing rapidly, fueled by global demand for advanced multimedia features. It’s a competitive space where giants like NVIDIA and Qualcomm push boundaries to cater to smartphones, smart homes, and automotive sectors. Asia-Pacific leads due to its massive consumer base and manufacturing strength, while challenges like supply chain issues persist. The market’s expansion reflects the world’s growing appetite for seamless, high-quality digital experiences across industries. Top driving factors include the boom in high-resolution content like 4K streaming and the rise of smart devices. Fast 5G networks enable real-time multimedia, while gaming and AR/VR push chipmakers to innovate. IoT growth and automotive infotainment systems also drive demand for powerful chipsets. These forces keep the market dynamic, as consumers expect ever-better performance from their devices.

Multimedia Chipsets Market size is expected to be worth around USD 52.1 Billion The Global Multimedia Chipsets Market size is expected to be worth around USD 52.1 Billion By 2034, from USD 29.9 billion in 2024, growing at a CAGR of 5.7% during the forecast period from 2025 to 2034. In 2024, APAC held a dominant market position, capturing more than a 43% share, holding USD 12.8 Billion revenue. Read more - https://market.us/report/global-multimedia-chipsets-market/ The Multimedia Chipsets Market is a vibrant industry centered on creating specialized chips that power audio, video, and graphics in devices like smartphones, TVs, and gaming consoles. These chipsets, including GPUs and SoCs, ensure smooth multimedia experiences, from streaming high-definition videos to rendering complex game graphics. They’re critical in consumer electronics, automotive systems, and IoT devices, meeting the rising need for rich digital content. This market thrives on innovation, with companies racing to deliver faster, more efficient chips for an increasingly connected world. The Multimedia Chipsets Market, as a market landscape, is growing rapidly, fueled by global demand for advanced multimedia features. It’s a competitive space where giants like NVIDIA and Qualcomm push boundaries to cater to smartphones, smart homes, and automotive sectors. Asia-Pacific leads due to its massive consumer base and manufacturing strength, while challenges like supply chain issues persist. The market’s expansion reflects the world’s growing appetite for seamless, high-quality digital experiences across industries. Top driving factors include the boom in high-resolution content like 4K streaming and the rise of smart devices. Fast 5G networks enable real-time multimedia, while gaming and AR/VR push chipmakers to innovate. IoT growth and automotive infotainment systems also drive demand for powerful chipsets. These forces keep the market dynamic, as consumers expect ever-better performance from their devices. -

-

Global Wireless Telecom Infrastructure Market Outlook (2024–2033): Evolution of Connectivity Across Networks Introduction The Global Wireless Telecom Infrastructure Market is projected to grow significantly, from USD 191.9 billion in 2023 to an estimated USD 502.3 billion by 2033, at a CAGR of 10.1%. This expansion is primarily driven by the surging demand for high-speed mobile internet, the rollout of 5G, and rapid urbanization. The increasing reliance on mobile connectivity for business, education, and entertainment is reshaping network infrastructure requirements. Asia-Pacific (APAC), with over 35% market share in 2023, led the global market, owing to its vast consumer base, supportive government initiatives, and strong telecom investments. https://market.us/report/wireless-telecom-infrastructure-industry-market/

-

-

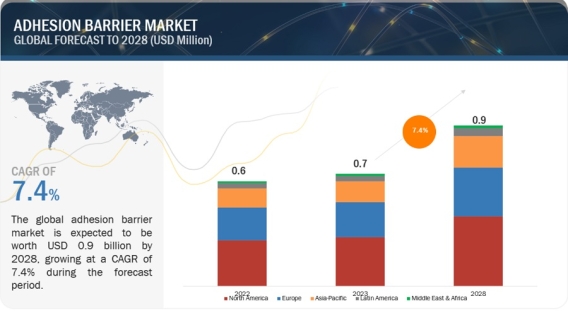

Global Adhesion Barrier Market Worth $0.9 Billion by 2028: Key Insights and Analysis https://www.marketsandmarkets.com/Market-Reports/adhesion-barrier-market-208132543.html The global adhesion barrier market size is projected to reach USD 0.9 billion by 2028 from USD 0.7 billion in 2023, at a CAGR of 7.4%. The main drivers driving the growth of this market are the increasing amount of surgeries and sports-related injuries, a growing elderly population, and increasing understanding of adhesion formation and conditions associated with adhesions. During the forecast period, this market's growth is anticipated to be constrained by surgeons' resistance to using adhesion barriers. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=208132543 Based on products, the adhesion barriers market is further segmented into synthetic and natural adhesion barriers. In 2022, the synthetic adhesion barriers segment accounted for the largest share of the adhesion barriers market. The large number of synthetic adhesion barriers that are commercially available and their higher utilisation by surgeons in various surgical procedures as compared to natural adhesion barriers can be attributed to the segment's growth. The sub-segment of synthetic adhesion barriers includes hyaluronic acid, regenerated cellulose, polyethylene glycol, and other synthetic adhesion barriers. Because they are biocompatible and bioresorbable, hyaluronic acid-based adhesion barriers have the largest market share in the synthetic adhesion barrier market. These are frequently used for open and laparoscopic general surgeries, including those involving the abdomen, pelvis, gynaecology, and other surgeries. Based on the type of formulation, the adhesion barriers market is segmented into film formulations, gel formulations, and liquid formulations. Given surgeon's increased preference for adhesion barriers in the form of films as well as the availability of clinical safety and efficacy data for these formulations, film formulations dominated the adhesion barrier market in 2022. Based on applications, General/Abdominal Surgeries surgeries held the largest share of the adhesion barriers market in 2022. A number of factors, including the increased risk of post-surgical adhesion formation in general/abdominal surgeries, the rising number of general/abdominal surgeries, and the availability of several commercialized adhesion barrier products for general/abdominal surgeries, can be attributed to the general/abdominal surgeries segment the large share of this market Based on end user, hospitals and clinics held the largest share of the adhesion barriers market in 2022. The largest share of this segment in the market of adhesion barrier is attributed to the large number of surgeries happening in the hospitals and clinics in both developed and developing countries. Geographically, the adhesion barriers market is segmented into North America, Europe, Asia Pacific, Latin America, and The Middle East and Africa. The North America's strong healthcare system, higher public and private expenditures on health care, growing numbers of the geriatric population, and an increasing prevalence of chronic and lifestyle diseases all contributed to North America having the largest share of the adhesion barrier market. On the other hand, the APAC market for adhesion barrier will expand due to factors like the rapidly growing geriatric population, the epidemiological shift from infectious to chronic diseases, and the rise in medical tourism. As a result, the APAC is anticipated to grow at a higher CAGR than other regions during the forecast period.

Global Adhesion Barrier Market Worth $0.9 Billion by 2028: Key Insights and Analysis https://www.marketsandmarkets.com/Market-Reports/adhesion-barrier-market-208132543.html The global adhesion barrier market size is projected to reach USD 0.9 billion by 2028 from USD 0.7 billion in 2023, at a CAGR of 7.4%. The main drivers driving the growth of this market are the increasing amount of surgeries and sports-related injuries, a growing elderly population, and increasing understanding of adhesion formation and conditions associated with adhesions. During the forecast period, this market's growth is anticipated to be constrained by surgeons' resistance to using adhesion barriers. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=208132543 Based on products, the adhesion barriers market is further segmented into synthetic and natural adhesion barriers. In 2022, the synthetic adhesion barriers segment accounted for the largest share of the adhesion barriers market. The large number of synthetic adhesion barriers that are commercially available and their higher utilisation by surgeons in various surgical procedures as compared to natural adhesion barriers can be attributed to the segment's growth. The sub-segment of synthetic adhesion barriers includes hyaluronic acid, regenerated cellulose, polyethylene glycol, and other synthetic adhesion barriers. Because they are biocompatible and bioresorbable, hyaluronic acid-based adhesion barriers have the largest market share in the synthetic adhesion barrier market. These are frequently used for open and laparoscopic general surgeries, including those involving the abdomen, pelvis, gynaecology, and other surgeries. Based on the type of formulation, the adhesion barriers market is segmented into film formulations, gel formulations, and liquid formulations. Given surgeon's increased preference for adhesion barriers in the form of films as well as the availability of clinical safety and efficacy data for these formulations, film formulations dominated the adhesion barrier market in 2022. Based on applications, General/Abdominal Surgeries surgeries held the largest share of the adhesion barriers market in 2022. A number of factors, including the increased risk of post-surgical adhesion formation in general/abdominal surgeries, the rising number of general/abdominal surgeries, and the availability of several commercialized adhesion barrier products for general/abdominal surgeries, can be attributed to the general/abdominal surgeries segment the large share of this market Based on end user, hospitals and clinics held the largest share of the adhesion barriers market in 2022. The largest share of this segment in the market of adhesion barrier is attributed to the large number of surgeries happening in the hospitals and clinics in both developed and developing countries. Geographically, the adhesion barriers market is segmented into North America, Europe, Asia Pacific, Latin America, and The Middle East and Africa. The North America's strong healthcare system, higher public and private expenditures on health care, growing numbers of the geriatric population, and an increasing prevalence of chronic and lifestyle diseases all contributed to North America having the largest share of the adhesion barrier market. On the other hand, the APAC market for adhesion barrier will expand due to factors like the rapidly growing geriatric population, the epidemiological shift from infectious to chronic diseases, and the rise in medical tourism. As a result, the APAC is anticipated to grow at a higher CAGR than other regions during the forecast period. -

-

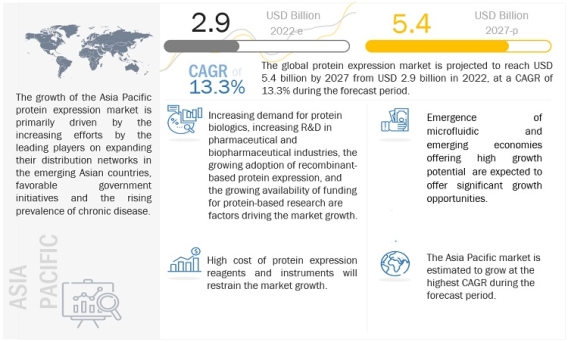

Unlocking the Potential of the $5.4 Billion Protein Expression Market https://www.marketsandmarkets.com/Market-Reports/protein-expression-market-180323924.html According to the new market research report "Protein Expression Market by Type (E.Coli, Mammalian, CHO, HEK 293, Insect, Pichia, Cell-free), Products (Reagents, Vectors, Competent Cells, Instruments, Service), Application (Therapeutic, Industrial), End User, and Region - Global Forecast to 2027", The global protein expression market is expected to reach USD 5.4 billion in 2027 from USD 2.9 billion in 2022 at a CAGR of 13.3% during the forecast period. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=180323924 Factors such as growing pharmaceutical and biotechnology industries, rising adoption of recombinant-based protein expression as well as increasing public and private support through initiatives and funding are favouring the growth of this market. However, the high cost of protein expression reagents and instruments is likely to restrain the growth of this market. Based on system type, the protein expression market is segmented into mammalian cell expression systems, prokaryotic expression systems, insect cell expression systems, yeast expression systems, cell-free expression systems, and algal-based expression systems. The mammalian cell expression systems segment accounted for the largest share of the global protein expression market in 2021. Based on application, the protein expression market is segmented into therapeutic, research and industrial applications. In 2021, the therapeutic applications segment accounted for the largest share of the global protein expression market. Factors such as an increase in protein-based research and the rising prevalence of chronic diseases across the globe contribute to the large share of this market. Based on product & service, the protein expression market is segmented into reagents, expression vectors, competent cells, instruments, and services. The reagents segment accounted for the largest share of the global protein expression market in 2021. Factors such as the increasing research activities in the field of protein expression as well as the large-scale production of antibodies and vaccines are responsible for large share of this market. Based on end users, the protein expression market is segmented into pharmaceutical and biotechnology companies, contract research organizations and contract development and manufacturing organizations (CROs and CDMOs), academic research institutes, and other end users. In 2021, the pharmaceutical and biotechnology companies segment accounted for the largest share of the global protein expression market due to an increase in protein research to understand biological systems and the rising production of recombinant therapeutic proteins for disease treatment. Geographical Growth Scenario: Based on region, the protein expression market is segmented into North America, Europe, Asia Pacific, Rest of the world (Latin America, and the Middle East & Africa). In 2021, North America accounted for the largest share of the global protein expression market, followed by Europe. Factors such as growth in the biotechnology and pharmaceutical industries, the rising prevalence of chronic disorders, and an increase in protein-based therapeutics research investments in the region contribute to its large share. The APAC market is projected to grow at the highest CAGR during the forecast period. Key Players: Thermo Fisher Scientific, Inc (US), Merck KGaA (Germany), GenScript Biotech Corporation (US), Agilent Technologies, Inc. (US), Takara Bio, Inc. (Japan), Bio-Rad Laboratories, Inc. (US), Qiagen N.V (Netherlands), Charles River Laboratories, Inc. (US), Danaher Corporation (US), Sartorius AG (Germany), Corning Incorporated (US), FUJIFILM Irvine Scientific, Inc. (Japan), Lonza Group AG (Switzerland), Bioneer Corporation (South Korea), Promega Corporation (US), Oxford Expression Technologies Ltd. (UK), ProteoGenix (France), Abeomics, Inc. (US), New England Biolabs, Inc. (US), Promab Biotechnologies (US), Sino Biological, Inc. (China), Jena Bioscience (Germany), Lifesensors, Inc. (US), Leading biology, Inc. (US), and Peak Proteins (UK). Recent Developments: In June 2021, Thermo Fisher Scientific Inc. (US) and Advanced Electrophoresis Solutions Ltd. (AES) (Canada) signed an agreement to combine essential protein separation techniques with mass spectrometry (MS) to advance therapeutic protein development through streamlined characterization. In June 2020, Lonza Group AG (Switzerland) launched GSv9, a chemically defined media and feeds platform specifically developed to enhance the performance of the GS Gene Expression System for optimized recombinant protein production.

Unlocking the Potential of the $5.4 Billion Protein Expression Market https://www.marketsandmarkets.com/Market-Reports/protein-expression-market-180323924.html According to the new market research report "Protein Expression Market by Type (E.Coli, Mammalian, CHO, HEK 293, Insect, Pichia, Cell-free), Products (Reagents, Vectors, Competent Cells, Instruments, Service), Application (Therapeutic, Industrial), End User, and Region - Global Forecast to 2027", The global protein expression market is expected to reach USD 5.4 billion in 2027 from USD 2.9 billion in 2022 at a CAGR of 13.3% during the forecast period. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=180323924 Factors such as growing pharmaceutical and biotechnology industries, rising adoption of recombinant-based protein expression as well as increasing public and private support through initiatives and funding are favouring the growth of this market. However, the high cost of protein expression reagents and instruments is likely to restrain the growth of this market. Based on system type, the protein expression market is segmented into mammalian cell expression systems, prokaryotic expression systems, insect cell expression systems, yeast expression systems, cell-free expression systems, and algal-based expression systems. The mammalian cell expression systems segment accounted for the largest share of the global protein expression market in 2021. Based on application, the protein expression market is segmented into therapeutic, research and industrial applications. In 2021, the therapeutic applications segment accounted for the largest share of the global protein expression market. Factors such as an increase in protein-based research and the rising prevalence of chronic diseases across the globe contribute to the large share of this market. Based on product & service, the protein expression market is segmented into reagents, expression vectors, competent cells, instruments, and services. The reagents segment accounted for the largest share of the global protein expression market in 2021. Factors such as the increasing research activities in the field of protein expression as well as the large-scale production of antibodies and vaccines are responsible for large share of this market. Based on end users, the protein expression market is segmented into pharmaceutical and biotechnology companies, contract research organizations and contract development and manufacturing organizations (CROs and CDMOs), academic research institutes, and other end users. In 2021, the pharmaceutical and biotechnology companies segment accounted for the largest share of the global protein expression market due to an increase in protein research to understand biological systems and the rising production of recombinant therapeutic proteins for disease treatment. Geographical Growth Scenario: Based on region, the protein expression market is segmented into North America, Europe, Asia Pacific, Rest of the world (Latin America, and the Middle East & Africa). In 2021, North America accounted for the largest share of the global protein expression market, followed by Europe. Factors such as growth in the biotechnology and pharmaceutical industries, the rising prevalence of chronic disorders, and an increase in protein-based therapeutics research investments in the region contribute to its large share. The APAC market is projected to grow at the highest CAGR during the forecast period. Key Players: Thermo Fisher Scientific, Inc (US), Merck KGaA (Germany), GenScript Biotech Corporation (US), Agilent Technologies, Inc. (US), Takara Bio, Inc. (Japan), Bio-Rad Laboratories, Inc. (US), Qiagen N.V (Netherlands), Charles River Laboratories, Inc. (US), Danaher Corporation (US), Sartorius AG (Germany), Corning Incorporated (US), FUJIFILM Irvine Scientific, Inc. (Japan), Lonza Group AG (Switzerland), Bioneer Corporation (South Korea), Promega Corporation (US), Oxford Expression Technologies Ltd. (UK), ProteoGenix (France), Abeomics, Inc. (US), New England Biolabs, Inc. (US), Promab Biotechnologies (US), Sino Biological, Inc. (China), Jena Bioscience (Germany), Lifesensors, Inc. (US), Leading biology, Inc. (US), and Peak Proteins (UK). Recent Developments: In June 2021, Thermo Fisher Scientific Inc. (US) and Advanced Electrophoresis Solutions Ltd. (AES) (Canada) signed an agreement to combine essential protein separation techniques with mass spectrometry (MS) to advance therapeutic protein development through streamlined characterization. In June 2020, Lonza Group AG (Switzerland) launched GSv9, a chemically defined media and feeds platform specifically developed to enhance the performance of the GS Gene Expression System for optimized recombinant protein production. -

-

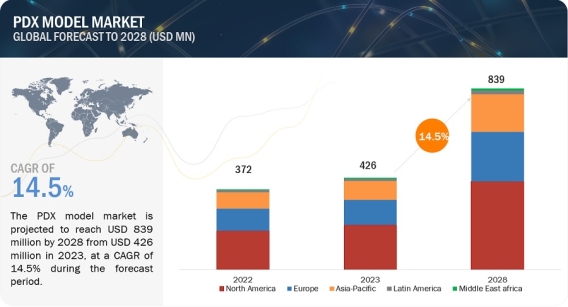

PDX Model Market Worth $839 Million: Opportunities and Challenges https://www.marketsandmarkets.com/Market-Reports/patient-derived-xenograft-model-market-121598251.html The PDX model market is projected to reach USD 839 million by 2028 from USD 426 million in 2023, at a CAGR of 14.5% during the forecast period. The key factors driving the growth of the global patient-derived xenograft/ PDX model market are the enhanced preclinical predictability, advancement of personalized medicine, and rise in the prevalence of cancer. However, ethical concerns surrounding the use of animal models along with high associated costs are expected to restrain market growth to a certain extent. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=121598251 The patient-derived xenograft/ PDX model market is categorized into five major categories: type, implantation method, tumor type, application, and end user. Based on type, the patient-derived xenograft/ PDX model market is segmented into mouse model and rat model. In 2023, the mouse model segment dominated the patient-derived xenograft/ PDX model market. Growth in this market segment can be attributed to biological similarities of the mice model with human tumors, and the availability of immunodeficient strains is expected to form the largest share segment in the patient-derived xenograft/ PDX model market. Based on implantation method, the market is categorized into subcutaneous implantation, orthotopic implantation, and other implantation methods. In 2023, the subcutaneous segment accounted for the largest share of the patient-derived xenografts/ PDX models market. The major drivers are propelling the accessibility and ease of Implantation of the subcutaneous method and the cost and time efficiency of the method. Based on tumor type, the patient-derived xenograft/ PDX model market is categorized into gastrointestinal tumor models, gynecological tumor models, respiratory tumor models, urological tumor models, hematological tumor models, and other tumor models. The hematological tumor models segment accounted for the fastest-growing segment of the tumor type segment of the patient-derived xenograft/ PDX model market. Market growth can largely be attributed to factors such a continuous rise in the incidence of hematological malignancies which is supporting research of treatments against hematological malignancies, and a growing focus on targeted therapies against cancer among others. Based on application, the patient-derived xenograft/ PDX model market is segmented into preclinical drug development, biomarker analysis, translational research, and biobanking. Among these, the preclinical drug development application segment accounted for the largest share of the patient-derived xenografts/ PDX models application market. The major driver fueling the growth of the patient-derived xenografts/ PDX models market is a constant increase in the number of ongoing clinical trials and the use of PDX models in the development of personalized therapeutic regimens for oncology treatments. Based on the end user, the segment is categorized into pharmaceutical & biotechnology companies, contract research organizations (CROs), and academic & research institutions. In 2023, the pharmaceutical and biotechnology companies segment dominated the end-user segment with the highest revenue share. Collaborative projects amongst the pharmaceutical and biotechnology companies, rising numbers of drugs in the R&D pipeline, and increasing investment in R&D are propelling the growth of the pharmaceutical and biotechnology companies market. Based on region, North America accounted for the largest share of the patient-derived xenografts/ PDX models market. The large share of the North American region can be attributed to extensive research focusing on novel oncology therapies, a rise in cancer prevalence, and increased adoption of personalized medicine. Moreover, the APAC region offers lucrative growth potential for the PDX models market. This can be attributed to the supportive regulatory framework, ongoing expansion and modernization of healthcare infrastructure across emerging Asian countries, and public-private initiatives to encourage awareness about personalized medicine. Major players operating in the patient-derived xenograft/ PDX model market include JSR Corporation (Japan), Wuxi Apptec (China), The Jackson Laboratory (US), Charles River Laboratories International, Inc. (US), Taconic Biosciences, Inc. (US), Oncodesign Precision Medicine (France), Inotiv, Inc. (US), Pharmatest Services (Finland), Hera BioLabs (US), EPO Berlin-Buch GmbH (Germany), Xentech (France), Urosphere (France), Altogen Labs (US), Abnova Corporation (US), Genesis Biotechnology Group (US), Biocytogen Pharmaceuticals Co., Ltd. (China), Creative Animodel (US), BioDuro-Sundia (US), Aragen Life Sciences (India), Shanghai LIDE Biotech Co., Ltd. (China), Certis Oncology Solutions (US), InnoSer (Netherlands), IVRS AB (Sweden), Beijing IDMO Co. Ltd. (China), and Shanghai Chempartner Co. Ltd. (China). Recent Developments in PDX Model Industry In December 2022, Crown Bioscience, Inc., a subsidiary of JSR Life Sciences, entered into a worldwide licensing agreement with ERS Genomics Limited. This agreement granted Crown Bioscience complete global access to ERS's foundational CRISPR/Cas9 patent portfolio, enabling the company to utilize CRISPR/Cas9 for genetic editing on a global scale. Under the provisions of this agreement, Crown Bioscience broadened its capabilities in genetic manipulation. The company is exploring the potential of gene editing within three-dimensional models of patient-derived tumor organoids. In July 2022, GemPharmatech entered into a strategic licensing arrangement with Charles River Laboratories, Inc. This partnership entails the exclusive distribution rights for GemPharmatech's advanced NOD CRISPR Prkdc Il2r gamma (NCG) mouse lines within the North American region. In November 2021, Inotiv announced the completion of the acquisition of Envigo RMS Holding Corp., a leading global provider of research models and services.

PDX Model Market Worth $839 Million: Opportunities and Challenges https://www.marketsandmarkets.com/Market-Reports/patient-derived-xenograft-model-market-121598251.html The PDX model market is projected to reach USD 839 million by 2028 from USD 426 million in 2023, at a CAGR of 14.5% during the forecast period. The key factors driving the growth of the global patient-derived xenograft/ PDX model market are the enhanced preclinical predictability, advancement of personalized medicine, and rise in the prevalence of cancer. However, ethical concerns surrounding the use of animal models along with high associated costs are expected to restrain market growth to a certain extent. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=121598251 The patient-derived xenograft/ PDX model market is categorized into five major categories: type, implantation method, tumor type, application, and end user. Based on type, the patient-derived xenograft/ PDX model market is segmented into mouse model and rat model. In 2023, the mouse model segment dominated the patient-derived xenograft/ PDX model market. Growth in this market segment can be attributed to biological similarities of the mice model with human tumors, and the availability of immunodeficient strains is expected to form the largest share segment in the patient-derived xenograft/ PDX model market. Based on implantation method, the market is categorized into subcutaneous implantation, orthotopic implantation, and other implantation methods. In 2023, the subcutaneous segment accounted for the largest share of the patient-derived xenografts/ PDX models market. The major drivers are propelling the accessibility and ease of Implantation of the subcutaneous method and the cost and time efficiency of the method. Based on tumor type, the patient-derived xenograft/ PDX model market is categorized into gastrointestinal tumor models, gynecological tumor models, respiratory tumor models, urological tumor models, hematological tumor models, and other tumor models. The hematological tumor models segment accounted for the fastest-growing segment of the tumor type segment of the patient-derived xenograft/ PDX model market. Market growth can largely be attributed to factors such a continuous rise in the incidence of hematological malignancies which is supporting research of treatments against hematological malignancies, and a growing focus on targeted therapies against cancer among others. Based on application, the patient-derived xenograft/ PDX model market is segmented into preclinical drug development, biomarker analysis, translational research, and biobanking. Among these, the preclinical drug development application segment accounted for the largest share of the patient-derived xenografts/ PDX models application market. The major driver fueling the growth of the patient-derived xenografts/ PDX models market is a constant increase in the number of ongoing clinical trials and the use of PDX models in the development of personalized therapeutic regimens for oncology treatments. Based on the end user, the segment is categorized into pharmaceutical & biotechnology companies, contract research organizations (CROs), and academic & research institutions. In 2023, the pharmaceutical and biotechnology companies segment dominated the end-user segment with the highest revenue share. Collaborative projects amongst the pharmaceutical and biotechnology companies, rising numbers of drugs in the R&D pipeline, and increasing investment in R&D are propelling the growth of the pharmaceutical and biotechnology companies market. Based on region, North America accounted for the largest share of the patient-derived xenografts/ PDX models market. The large share of the North American region can be attributed to extensive research focusing on novel oncology therapies, a rise in cancer prevalence, and increased adoption of personalized medicine. Moreover, the APAC region offers lucrative growth potential for the PDX models market. This can be attributed to the supportive regulatory framework, ongoing expansion and modernization of healthcare infrastructure across emerging Asian countries, and public-private initiatives to encourage awareness about personalized medicine. Major players operating in the patient-derived xenograft/ PDX model market include JSR Corporation (Japan), Wuxi Apptec (China), The Jackson Laboratory (US), Charles River Laboratories International, Inc. (US), Taconic Biosciences, Inc. (US), Oncodesign Precision Medicine (France), Inotiv, Inc. (US), Pharmatest Services (Finland), Hera BioLabs (US), EPO Berlin-Buch GmbH (Germany), Xentech (France), Urosphere (France), Altogen Labs (US), Abnova Corporation (US), Genesis Biotechnology Group (US), Biocytogen Pharmaceuticals Co., Ltd. (China), Creative Animodel (US), BioDuro-Sundia (US), Aragen Life Sciences (India), Shanghai LIDE Biotech Co., Ltd. (China), Certis Oncology Solutions (US), InnoSer (Netherlands), IVRS AB (Sweden), Beijing IDMO Co. Ltd. (China), and Shanghai Chempartner Co. Ltd. (China). Recent Developments in PDX Model Industry In December 2022, Crown Bioscience, Inc., a subsidiary of JSR Life Sciences, entered into a worldwide licensing agreement with ERS Genomics Limited. This agreement granted Crown Bioscience complete global access to ERS's foundational CRISPR/Cas9 patent portfolio, enabling the company to utilize CRISPR/Cas9 for genetic editing on a global scale. Under the provisions of this agreement, Crown Bioscience broadened its capabilities in genetic manipulation. The company is exploring the potential of gene editing within three-dimensional models of patient-derived tumor organoids. In July 2022, GemPharmatech entered into a strategic licensing arrangement with Charles River Laboratories, Inc. This partnership entails the exclusive distribution rights for GemPharmatech's advanced NOD CRISPR Prkdc Il2r gamma (NCG) mouse lines within the North American region. In November 2021, Inotiv announced the completion of the acquisition of Envigo RMS Holding Corp., a leading global provider of research models and services. -

-

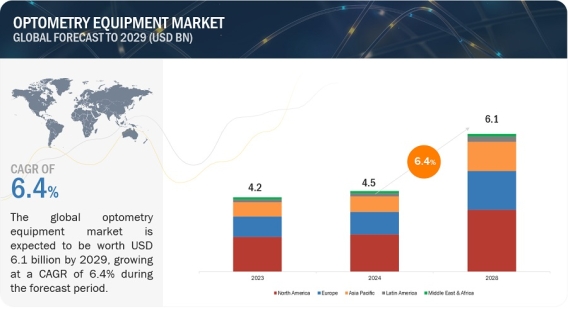

Future Trends: Optometry Equipment Market Poised for $6.1 Billion by 2029 https://www.marketsandmarkets.com/Market-Reports/optometry-eye-exam-equipment-market-14475790.html The global optometry equipment market is valued at an estimated USD 4.5 billion in 2024 and is projected to reach USD 6.1 billion by 2029, at a CAGR of 6.4% during the forecast period. The three main factors propelling the growth of the optometry equipment market are the aging population, the rise in eye illnesses, and the rising cost of healthcare in emerging nations. The retina and glaucoma examination products, general examination products, and cornea and cataract examination products comprise the type-based segments of the worldwide optometry equipment market. During the projected period, the optometry equipment market, with its focus on retina and glaucoma examination items, is anticipated to have the greatest growth rate and market share. This segment is growing at a significant rate mostly because to an increase in glaucoma and retinal illnesses. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=14475790 Based on application, the optometry equipment market is divided into categories such as general examination, cataract, glaucoma, age-related macular degeneration, and other applications. Over the course of the projection period, the general examination category is anticipated to have a larger market share. In the upcoming years, factors including the growing prevalence of eye illnesses and the increased awareness of eye care are anticipated to fuel market expansion. Hospitals, eye clinics, and other end users comprise the end user segment of the optometry equipment market. In terms of worldwide market share for optometry equipment in 2023, the clinics sector led. The segment's market share is influenced by a large patient pool that is treated in clinics, an increasing number of private clinics and practitioners in emerging countries, and an increase in the prevalence of visual impairments among the elderly. The optometry equipment market is segmented into four major regions—North America, Europe, the Asia Pacific and Rest of the World (Latin America, the Middle East & Africa and GCC Countries). Over the course of the forecast period, the Asia Pacific market is anticipated to develop at the greatest CAGR. The rising incidence of ocular illnesses, rising healthcare spending in certain APAC nations, and the existence of high-growing markets in the area are all factors contributing to this market's rise. The positive regulatory climate in this area is also anticipated to fuel market expansion. Carl Zeiss Meditec AG (Germany), Alcon (Switzerland), EssilorLuxottica (France), Topcon Corporation (Japan), Bausch Health Companies Inc. (Canada), NIDEK Co. Ltd. (Japan), Canon Inc. (Japan), Johnson and Johnson (US), HEINE Optotechnik (Germany), Revenio Group PLC (Finland), Haag-Streit Group (Switzerland), Heidelberg Engineering (Germany), Luneau Technology (France), Escalon Medical (US), Keeler Ltd. (UK), Reichert Technologies (US), Oculus Inc. (US), Kowa American Corporation (US), Ziemer Ophthalmic Systems AG (Switzerland), Huvitz (South Korea), Neitz Instruments Co. Ltd. (Japan), Rexxam Co. Ltd. (Japan), Rudolf-Riester GmbH (Germany), FREY (Poland), and Yeasn (China) Recent Developments of Optometry Equipment Industry: In August 2023, Carl Zeiss launched the ZEISS trifocal technology on a glistening-free hydrophobic C-loop platform and a fully preloaded injector for safe and reliable implantation. In March 2022, Topcon Corporation launched SOLOS, an automatic lens analyzer that enables advanced, accurate, and efficient lens analysis at the touch of a button. In September 2023, Bauch + Lomb acquired XIIDRA to grow in the prescription dry eyes segment. In January 2023Bausch + Lomb acquired AcuFocus to expand its cataract surgical portfolio.

Future Trends: Optometry Equipment Market Poised for $6.1 Billion by 2029 https://www.marketsandmarkets.com/Market-Reports/optometry-eye-exam-equipment-market-14475790.html The global optometry equipment market is valued at an estimated USD 4.5 billion in 2024 and is projected to reach USD 6.1 billion by 2029, at a CAGR of 6.4% during the forecast period. The three main factors propelling the growth of the optometry equipment market are the aging population, the rise in eye illnesses, and the rising cost of healthcare in emerging nations. The retina and glaucoma examination products, general examination products, and cornea and cataract examination products comprise the type-based segments of the worldwide optometry equipment market. During the projected period, the optometry equipment market, with its focus on retina and glaucoma examination items, is anticipated to have the greatest growth rate and market share. This segment is growing at a significant rate mostly because to an increase in glaucoma and retinal illnesses. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=14475790 Based on application, the optometry equipment market is divided into categories such as general examination, cataract, glaucoma, age-related macular degeneration, and other applications. Over the course of the projection period, the general examination category is anticipated to have a larger market share. In the upcoming years, factors including the growing prevalence of eye illnesses and the increased awareness of eye care are anticipated to fuel market expansion. Hospitals, eye clinics, and other end users comprise the end user segment of the optometry equipment market. In terms of worldwide market share for optometry equipment in 2023, the clinics sector led. The segment's market share is influenced by a large patient pool that is treated in clinics, an increasing number of private clinics and practitioners in emerging countries, and an increase in the prevalence of visual impairments among the elderly. The optometry equipment market is segmented into four major regions—North America, Europe, the Asia Pacific and Rest of the World (Latin America, the Middle East & Africa and GCC Countries). Over the course of the forecast period, the Asia Pacific market is anticipated to develop at the greatest CAGR. The rising incidence of ocular illnesses, rising healthcare spending in certain APAC nations, and the existence of high-growing markets in the area are all factors contributing to this market's rise. The positive regulatory climate in this area is also anticipated to fuel market expansion. Carl Zeiss Meditec AG (Germany), Alcon (Switzerland), EssilorLuxottica (France), Topcon Corporation (Japan), Bausch Health Companies Inc. (Canada), NIDEK Co. Ltd. (Japan), Canon Inc. (Japan), Johnson and Johnson (US), HEINE Optotechnik (Germany), Revenio Group PLC (Finland), Haag-Streit Group (Switzerland), Heidelberg Engineering (Germany), Luneau Technology (France), Escalon Medical (US), Keeler Ltd. (UK), Reichert Technologies (US), Oculus Inc. (US), Kowa American Corporation (US), Ziemer Ophthalmic Systems AG (Switzerland), Huvitz (South Korea), Neitz Instruments Co. Ltd. (Japan), Rexxam Co. Ltd. (Japan), Rudolf-Riester GmbH (Germany), FREY (Poland), and Yeasn (China) Recent Developments of Optometry Equipment Industry: In August 2023, Carl Zeiss launched the ZEISS trifocal technology on a glistening-free hydrophobic C-loop platform and a fully preloaded injector for safe and reliable implantation. In March 2022, Topcon Corporation launched SOLOS, an automatic lens analyzer that enables advanced, accurate, and efficient lens analysis at the touch of a button. In September 2023, Bauch + Lomb acquired XIIDRA to grow in the prescription dry eyes segment. In January 2023Bausch + Lomb acquired AcuFocus to expand its cataract surgical portfolio. -

-

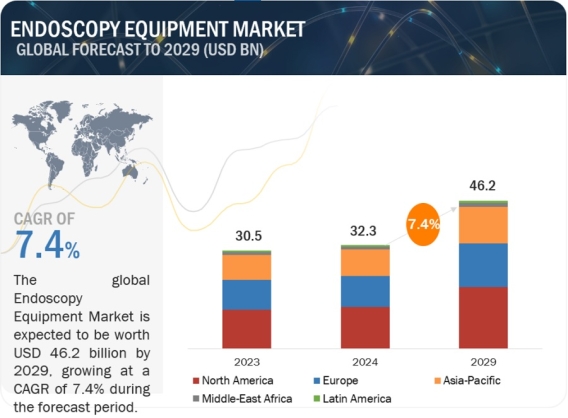

Market Surge: Endoscopy Equipment Expected to Hit $46.2 Billion by 2029 https://www.marketsandmarkets.com/Market-Reports/endoscopy-devices-market-689.html The global endoscopy equipment market is projected to reach USD 46.2 billion by 2029 from USD 32.3 billion in 2024, at a CAGR of 7.4%. The global endoscopy equipment market is experiencing substantial growth due to many driving factors, including surging requirement for endoscopy to diagnose and treat target diseases, increasing investments, funds, and grants by governments and other organizations worldwide, growing focus of hospitals to invest in technology advanced endoscopy instruments and expand endoscopy units, ongoing advancements in endoscopic technologies to ensure patient safety and achieve more accurate treatments, rising incidence of IBD and CRC that require endoscopy procedures. Drivers such as Increasing preference for minimally invasive surgeries, adoption of single-use endoscopy instruments to prevent infectious diseases and offer increased efficiency and safety, and rising focus of medical specialities to shift from manual to automated endoscopy reprocessing are also contributing towards the overall growth of the global endoscopy equipment market. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=689 Endoscopy Equipment Market by Product (Endoscope (Flexible, Disposible, Rigid, Capsule, Robot-assisted), Visualization Systems (Video Converters, Recorders, Processors)), Application, End User, and Region - Global Forecast to 2029 In this report, the endoscopy equipment market is segmented into product type, application type, end user, and region. Based on product type, the endoscopy equipment market is divided into endoscopes, visualization systems, other endoscopy equipment, and accessories. As of 2023, the accessories segment accounted the third largest share in the global endoscopy equipment market.The market share can be attributed to the factors that there are a side variety of accessories designed for specific procedures and functionalities and they are compatible with various models from the manufacturers.. Based on the type of applications, the endoscopy equipment market includes segments such as gastrointestinal endoscopy, laparoscopy, arthroscopy, obstetrics/gynecology endoscopy, urology endoscopy, bronchoscopy, mediastinoscopy, ENT endoscopy, and other specialized applications. Among these, the arthroscopy segment accounted the fourth largest share of the overall endoscopy equipment market in 2023. This dominance is primarily attributed to demographic shifts, particularly the aging population in key regions like the US, China, Japan, and India. Additionally, the increased prevalence of joint injuries like ligament tears, meniscus damange, and rotator cuff injuriesamong younger adults has heightened awareness about the importance of arthroscopy, contributing to the segment's significant growth rate. Based on end users, the endoscopy equipment market is segmented into hospitals, ambulatory surgery centers/clinics and other end user. The other end user segment accounted for the third largest share in the endoscopy equipment market in 2023. This dominance can be attributed to several driving factors. Diagnostic Laboratories, Research Institutions has nowadays started to implement new technologies and advanced procedures. Additionally, the increasing prevalence of complex medical conditions requiring diagnostic endoscopic procedures further amplifies the demand for such equipment within diagnostic centers, solidifying their position in this market. Based on the regions, in 2023, North America emerged as the dominant region in the endoscopy equipment market, followed by Europe, APAC, Latin America and Middle East and Africa. This leadership position is owed to substantial investments made by hospitals towards procuring advanced endoscopic equipment, coupled with a strong emphasis on research aimed at refining endoscopy techniques. Additionally, favorable reimbursement policies for endoscopic procedures in the US and the adoption of innovative funding models by hospitals in Canada further bolstered the region's prominence. Meanwhile, in the Asia Pacific market, particularly in China and India, a higher compound annual growth rate (CAGR) is anticipated throughout the forecast period. This growth trajectory is underpinned by various factors including escalating demand for minimally invasive surgical procedures, rising healthcare expenditure, the proliferation of hospitals, an expanding patient population, continuous improvements in healthcare infrastructure, and supportive government policies promoting the use of single-use endoscopy devices. Notably, leading market players are strategically focusing on launching new products and enhancing existing ones to fortify their product portfolios and expand their distribution networks. Prominent players in the endoscopy equipment market include Olympus Corporation (Japan), KARL STORZ SE & Co. KG (Germany), Boston Scientific Corporation (US), JOHNSON & JOHNSON (US), Stryker Corporation (US), Medtronic, plc (Ireland), Fujifilm Holdings Corporation (Japan), HOYA Corporation (Japan), Nipro Corporation (Japan), Smith & Nephew plc (UK), Intuitive Surgical, Inc. (US) Recent Developments of Endoscopy Equipment Industry: In November 2023, Olympus Corporation launched the EVIS X1, an advanced endoscopy system in the existing product portfolio of the company.. In September 2023, Stryker launched, 1788, a minimally invasive surgical camera, offering more vibrant image with balanced lighting. In January 2022, The Johnson & Johnson Medical Devices Companies (JJMDC) collaborated with Microsoft Corporation Inc, (US) to enable and expand JJMDC’s secure and compliant digital surgery ecosystem.

Market Surge: Endoscopy Equipment Expected to Hit $46.2 Billion by 2029 https://www.marketsandmarkets.com/Market-Reports/endoscopy-devices-market-689.html The global endoscopy equipment market is projected to reach USD 46.2 billion by 2029 from USD 32.3 billion in 2024, at a CAGR of 7.4%. The global endoscopy equipment market is experiencing substantial growth due to many driving factors, including surging requirement for endoscopy to diagnose and treat target diseases, increasing investments, funds, and grants by governments and other organizations worldwide, growing focus of hospitals to invest in technology advanced endoscopy instruments and expand endoscopy units, ongoing advancements in endoscopic technologies to ensure patient safety and achieve more accurate treatments, rising incidence of IBD and CRC that require endoscopy procedures. Drivers such as Increasing preference for minimally invasive surgeries, adoption of single-use endoscopy instruments to prevent infectious diseases and offer increased efficiency and safety, and rising focus of medical specialities to shift from manual to automated endoscopy reprocessing are also contributing towards the overall growth of the global endoscopy equipment market. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=689 Endoscopy Equipment Market by Product (Endoscope (Flexible, Disposible, Rigid, Capsule, Robot-assisted), Visualization Systems (Video Converters, Recorders, Processors)), Application, End User, and Region - Global Forecast to 2029 In this report, the endoscopy equipment market is segmented into product type, application type, end user, and region. Based on product type, the endoscopy equipment market is divided into endoscopes, visualization systems, other endoscopy equipment, and accessories. As of 2023, the accessories segment accounted the third largest share in the global endoscopy equipment market.The market share can be attributed to the factors that there are a side variety of accessories designed for specific procedures and functionalities and they are compatible with various models from the manufacturers.. Based on the type of applications, the endoscopy equipment market includes segments such as gastrointestinal endoscopy, laparoscopy, arthroscopy, obstetrics/gynecology endoscopy, urology endoscopy, bronchoscopy, mediastinoscopy, ENT endoscopy, and other specialized applications. Among these, the arthroscopy segment accounted the fourth largest share of the overall endoscopy equipment market in 2023. This dominance is primarily attributed to demographic shifts, particularly the aging population in key regions like the US, China, Japan, and India. Additionally, the increased prevalence of joint injuries like ligament tears, meniscus damange, and rotator cuff injuriesamong younger adults has heightened awareness about the importance of arthroscopy, contributing to the segment's significant growth rate. Based on end users, the endoscopy equipment market is segmented into hospitals, ambulatory surgery centers/clinics and other end user. The other end user segment accounted for the third largest share in the endoscopy equipment market in 2023. This dominance can be attributed to several driving factors. Diagnostic Laboratories, Research Institutions has nowadays started to implement new technologies and advanced procedures. Additionally, the increasing prevalence of complex medical conditions requiring diagnostic endoscopic procedures further amplifies the demand for such equipment within diagnostic centers, solidifying their position in this market. Based on the regions, in 2023, North America emerged as the dominant region in the endoscopy equipment market, followed by Europe, APAC, Latin America and Middle East and Africa. This leadership position is owed to substantial investments made by hospitals towards procuring advanced endoscopic equipment, coupled with a strong emphasis on research aimed at refining endoscopy techniques. Additionally, favorable reimbursement policies for endoscopic procedures in the US and the adoption of innovative funding models by hospitals in Canada further bolstered the region's prominence. Meanwhile, in the Asia Pacific market, particularly in China and India, a higher compound annual growth rate (CAGR) is anticipated throughout the forecast period. This growth trajectory is underpinned by various factors including escalating demand for minimally invasive surgical procedures, rising healthcare expenditure, the proliferation of hospitals, an expanding patient population, continuous improvements in healthcare infrastructure, and supportive government policies promoting the use of single-use endoscopy devices. Notably, leading market players are strategically focusing on launching new products and enhancing existing ones to fortify their product portfolios and expand their distribution networks. Prominent players in the endoscopy equipment market include Olympus Corporation (Japan), KARL STORZ SE & Co. KG (Germany), Boston Scientific Corporation (US), JOHNSON & JOHNSON (US), Stryker Corporation (US), Medtronic, plc (Ireland), Fujifilm Holdings Corporation (Japan), HOYA Corporation (Japan), Nipro Corporation (Japan), Smith & Nephew plc (UK), Intuitive Surgical, Inc. (US) Recent Developments of Endoscopy Equipment Industry: In November 2023, Olympus Corporation launched the EVIS X1, an advanced endoscopy system in the existing product portfolio of the company.. In September 2023, Stryker launched, 1788, a minimally invasive surgical camera, offering more vibrant image with balanced lighting. In January 2022, The Johnson & Johnson Medical Devices Companies (JJMDC) collaborated with Microsoft Corporation Inc, (US) to enable and expand JJMDC’s secure and compliant digital surgery ecosystem. -

-

Discover the Power of Plotter Printer Machines for Your Business Unlock the full potential of your business with the cutting-edge technology of Plotter Printer Machines. These versatile machines go beyond traditional printing, offering large-format, high-quality output for a wide range of applications. From vibrant signage and banners to detailed technical drawings and architectural plans, Plotter Printer Machines deliver unparalleled precision and clarity. Streamline your workflow, enhance your brand visibility, and unlock new revenue streams by investing in these powerful tools. Discover how Plotter Printer Machines can transform your business operations and propel you towards greater success. Explore the latest models, features, and capabilities to find the perfect fit for your unique needs. Unlock a world of possibilities and take your business to new heights with the power of Plotter Printer Machines. Visit: - https://cricutindiastore.com/product/cricut-explore-3-apac/

-

-

The database management systems category is expected to grow at a CAGR of 12.05% from 2023 to 2030. North America has the biggest category share and APAC is expected to be the fastest growing region during the forecast period. The growing adoption of advanced technologies is fueling the growth of database management systems (DBMS). https://industrysurvey.wordpress.com/2024/05/30/top-trends-shaping-the-database-management-systems-procurement-intelligence/

-

-

The clinical IT services category is expected to grow at a CAGR of 17.9% from 2023 to 2030. North America has the biggest category share with more than 50% and APAC is expected to be the fastest-growing region during the forecast period. https://industrysurvey.wordpress.com/2024/05/28/embracing-innovation-clinical-it-services-procurement-trends-to-watch-in-2030/

Copyright 2019 © P-tweets Refunds