199 results found | searching for "korea"

-

-

The global Bioprocess Bags Market was valued at USD 3.50 billion in 2023 and is projected to reach USD 13.78 billion by 2032, growing at an impressive CAGR of 16.46% between 2024 and 2032. This remarkable growth reflects the surging adoption of single-use technologies across the biopharmaceutical sector, where efficiency, scalability, and contamination control have become essential for both research and large-scale drug production. Bioprocess bags are critical tools for storage, mixing, and transport of biopharmaceutical fluids, offering superior sterility and reducing the risks associated with traditional stainless-steel systems. Their increasing integration into upstream and downstream processing highlights a transformative shift in the way biologics, vaccines, and cell-based therapies are developed and manufactured. Market Dynamics: Why the Industry Is Scaling at Unprecedented Levels The rapid expansion of biologics and biosimilars pipelines worldwide is a major force fueling the demand for bioprocess bags. As pharmaceutical companies face heightened pressure to bring therapies to market quickly, flexible and reliable solutions like bioprocess bags offer significant advantages. They lower capital costs, reduce cleaning validation requirements, and minimize the risk of cross-contamination. Furthermore, the COVID-19 pandemic accelerated the acceptance of single-use technologies. Manufacturers worldwide experienced firsthand the flexibility these systems provided in ramping up vaccine production. That momentum continues to shape bioprocessing strategies, with companies investing heavily in disposable solutions to ensure agility and speed. Bioprocess bags are not just limited to large-scale manufacturing. They are increasingly being adopted in academic research labs, contract development and manufacturing organizations (CDMOs), and emerging biotech startups, where scalability and cost-effectiveness are equally critical. Technological Advancements Enhancing Market Potential The bioprocess bags industry is witnessing significant innovation in materials, design, and performance. Leading manufacturers are focusing on developing multilayer films that provide enhanced durability, high oxygen barrier properties, and compatibility with a wide range of biologic materials. Additionally, bags are being designed with advanced monitoring systems that integrate sensors to track pH, dissolved oxygen, and other key parameters in real time. These smart bag solutions align with the biopharma industry’s push toward process intensification and continuous manufacturing. The development of customizable and scalable bag formats is further supporting small- and mid-sized biotech firms that require flexibility without compromising compliance with regulatory standards. Regional Outlook: North America and Asia-Pacific at the Forefront North America continues to lead the bioprocess bags market, driven by the strong presence of biopharmaceutical giants, advanced research infrastructure, and favorable regulatory frameworks. The region’s focus on biologics, particularly monoclonal antibodies and gene therapies, sustains robust demand for single-use solutions. Meanwhile, Asia-Pacific is emerging as a hotspot for growth. Rapidly expanding biotech clusters in countries like China, India, and South Korea are attracting global investments. Governments in the region are promoting domestic biologics production, further boosting adoption of bioprocess bags. The lower cost of production combined with strong demand for biosimilars positions Asia-Pacific as a key growth engine for the forecast period. Key Market Drivers Booming Biologics and Biosimilars Market: Rising prevalence of chronic diseases and demand for advanced therapies have placed biologics at the center of global healthcare, propelling the need for reliable bioprocessing solutions. Shift Toward Single-Use Technologies: The move away from stainless-steel systems to disposable bags significantly reduces downtime, contamination risks, and operational costs. Growing Investment in Cell and Gene Therapy: Breakthroughs in regenerative medicine demand flexible and sterile solutions that bioprocess bags are uniquely designed to provide. Rapid Expansion of Contract Manufacturing Organizations: As CDMOs scale operations globally, the reliance on single-use technologies becomes indispensable. Competitive Landscape The bioprocess bags market is highly competitive with a mix of global leaders and specialized niche players. Companies are focusing on collaborations, acquisitions, and product launches to strengthen their portfolios. Leading players are also investing in expanding production capacities to meet the surging global demand. Recent trends show a rise in partnerships between suppliers and CDMOs to co-develop customized solutions. Such collaborations enable end-users to achieve process efficiencies while ensuring compliance with regulatory standards. Challenges to Watch Despite its strong trajectory, the market does face hurdles. Concerns related to leachables and extractables from plastic materials remain under scrutiny, particularly from regulatory authorities. Additionally, supply chain disruptions for raw materials can pose risks to production continuity. However, industry stakeholders are addressing these challenges through rigorous testing protocols, improved material science, and diversification of supply chains to ensure consistent availability of high-quality bioprocess bags. Future Outlook The bioprocess bags market is positioned for exceptional growth throughout the next decade. The convergence of biologics expansion, single-use adoption, and smart technology integration sets the stage for continued innovation. With advancements in material engineering and automation, bioprocess bags are expected to evolve from simple storage tools to highly sophisticated components that actively support biomanufacturing. As the healthcare industry shifts toward precision medicine, biologics and cell-based therapies will demand even greater flexibility and sterility in manufacturing processes. Bioprocess bags are uniquely aligned to meet these evolving needs, cementing their role as a cornerstone of modern bioprocessing. Industry analysts predict that the next phase of growth will be marked by hybrid systems, where single-use technologies like bioprocess bags coexist with stainless-steel infrastructure to optimize performance, scalability, and sustainability. Conclusion With a projected market value of USD 13.78 billion by 2032, the bioprocess bags industry is set to reshape the global biopharmaceutical manufacturing landscape. Its rapid adoption underscores the industry’s commitment to efficiency, sterility, and adaptability in an increasingly competitive market environment. For stakeholders across the value chain, from biotech startups to global pharmaceutical leaders, investing in bioprocess bag solutions represents not just an operational advantage but a strategic imperative. Read More: https://www.snsinsider.com/reports/bioprocess-bags-market-6853

-

-

Semiconductor Filter Market size is expected to be worth around USD 3,062.7 MN The Global Semiconductor Filter Market size is expected to be worth around USD 3,062.7 Million By 2034, from USD 1,293.7 Million in 2024, growing at a CAGR of 9.00% during the forecast period from 2025 to 2034. Asia-Pacific dominated the semiconductor filter industry in 2024, accounting for over 49% of the market share and generating USD 633 Million in revenue. Read more - https://market.us/report/semiconductor-filter-market/ The Semiconductor Filter Market refers to the industry focused on producing and supplying specialized filtration systems used in semiconductor manufacturing. These filters are critical for maintaining ultra-clean environments by removing contaminants like particles, gases, and chemicals from air, liquids, and gases used in processes such as photolithography, etching, and chemical mechanical planarization. The market caters to the semiconductor industry’s need for high-purity conditions to ensure the quality and reliability of chips, which are integral to electronics, automotive, telecommunications, and healthcare sectors. As chips become smaller and more complex, the demand for advanced filtration solutions grows, driven by the need for precision and defect-free production. This market includes various filter types, such as air, liquid, and gas filters, each designed to meet stringent industry standards. The market size for semiconductor filters has been expanding steadily, with estimates suggesting it was valued at around USD 1.7 billion in 2024 and is projected to grow significantly over the next decade, potentially reaching USD 3.56 billion by 2033 at a compound annual growth rate (CAGR) of 8.5%. This growth is fueled by the increasing complexity of semiconductor manufacturing, particularly for advanced nodes like 7nm and below, which require ultra-pure environments. The Asia-Pacific region dominates due to its robust semiconductor manufacturing base in countries like China, Taiwan, South Korea, and Japan. North America also holds a significant share, driven by major players like Intel and Global Foundries. The market’s expansion is supported by rising demand for consumer electronics, automotive semiconductors, and emerging technologies like 5G and IoT.

Semiconductor Filter Market size is expected to be worth around USD 3,062.7 MN The Global Semiconductor Filter Market size is expected to be worth around USD 3,062.7 Million By 2034, from USD 1,293.7 Million in 2024, growing at a CAGR of 9.00% during the forecast period from 2025 to 2034. Asia-Pacific dominated the semiconductor filter industry in 2024, accounting for over 49% of the market share and generating USD 633 Million in revenue. Read more - https://market.us/report/semiconductor-filter-market/ The Semiconductor Filter Market refers to the industry focused on producing and supplying specialized filtration systems used in semiconductor manufacturing. These filters are critical for maintaining ultra-clean environments by removing contaminants like particles, gases, and chemicals from air, liquids, and gases used in processes such as photolithography, etching, and chemical mechanical planarization. The market caters to the semiconductor industry’s need for high-purity conditions to ensure the quality and reliability of chips, which are integral to electronics, automotive, telecommunications, and healthcare sectors. As chips become smaller and more complex, the demand for advanced filtration solutions grows, driven by the need for precision and defect-free production. This market includes various filter types, such as air, liquid, and gas filters, each designed to meet stringent industry standards. The market size for semiconductor filters has been expanding steadily, with estimates suggesting it was valued at around USD 1.7 billion in 2024 and is projected to grow significantly over the next decade, potentially reaching USD 3.56 billion by 2033 at a compound annual growth rate (CAGR) of 8.5%. This growth is fueled by the increasing complexity of semiconductor manufacturing, particularly for advanced nodes like 7nm and below, which require ultra-pure environments. The Asia-Pacific region dominates due to its robust semiconductor manufacturing base in countries like China, Taiwan, South Korea, and Japan. North America also holds a significant share, driven by major players like Intel and Global Foundries. The market’s expansion is supported by rising demand for consumer electronics, automotive semiconductors, and emerging technologies like 5G and IoT. -

-

South Korea Cloud Computing Market: Why is It Increasingly Important? The implementation of South Korea cloud computing market through various initiatives. They are allocating funds in the development of a strong cloud infrastructure including sophisticated data centers. It is to eventually establish a dependable and effective business environment. Fore more info:- https://www.pageorama.com/?p=southkoreacloudcomputingmarket

-

-

South Korea Cloud Computing Market Trends 2031: As we approach 2031, the South Korea Cloud Computing Market is poised for substantial growth and transformation. With technological advancements and evolving business needs driving the market, understanding the key trends is essential for stakeholders looking to navigate this dynamic landscape. Fore more info:- https://www.rueami.com/2024/07/20/the-south-korea-cloud-computing-market-in-2031-emerging-trends-and-opportunities/

-

-

Is Glass Skin Possible for You? The desired "glass skin" fad has swept the beauty industry. It exemplifies perfect skin with its smooth, transparent, and virtually poreless complexion that exudes a healthy glow. However, while the notion and appearance of glass skin are widespread in Korea, is the same true for other nationalities? Is glass skin look feasible for everyone, or is it merely a K-beauty fantasy? In this comprehensive guide from AAYNA, we'll go over everything you need to know to achieve Glass Skin. Almost everyone can achieve glass skin, but it takes a combination of expert treatments and a consistent at-home skincare regimen. Beyond at-home care, understanding your skin's chemistry and recognizing what is lacking is also critical. At AAYNA Clinic, our doctors and aestheticians work with you to develop and implement a skincare routine that will help your skin restore and maintain hydration, brightness, and smoothness. To schedule your consultation, please contact our team or visit our website for additional information. https://www.aaynaclinic.com/is-glass-skin-possible-for-you/

-

-

Samsung will soon let you create AI wallpapers on its touchscreen refrigerators Samsung has announced new AI capabilities for its smart appliances, including new AI-generated wallpapers for certain refrigerators, as well as an AI upgrade for its Bixby voice assistant. The updated Bixby will hit five Samsung Bespoke appliances starting on August 27th. AI-generated wallpapers are coming to Samsung Family Hub refrigerators released in the US and Korea after 2022, the company says. To create them, users will pick a theme from seven categories and one of six art styles. Once the new wallpaper is created, it can go on the fridge’s cover screen or whiteboard, or saved in an album for later. It will require a Wi-Fi connection, and users will be limited to creating up to five wallpapers per day. https://www.theverge.com/2024/8/26/24228788/samsung-ai-wallpapers-refrigerators-bixby-upgrade-bespoke-appliances

-

-

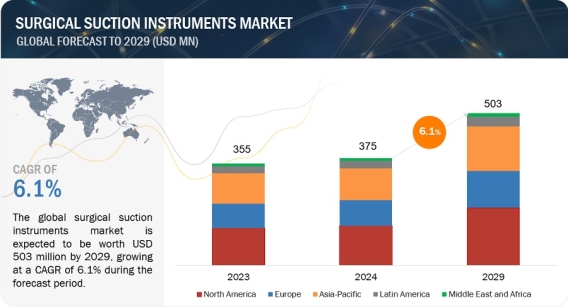

Innovations and Opportunities in the $503 Million Surgical Suction Instruments Market by 2029 https://www.marketsandmarkets.com/Market-Reports/surgical-suction-instruments-market-129636225.html The global surgical suction instruments market is projected to reach 503 million in 2029 from USD 375 million in 2024, at a CAGR of 6.1% between 2024 and 2029. The rising technological advancemnets and increasing geriatric population is driving the growth of the market. As the global population ages, the number of chronic diseases is increasing which is expected to drive the market growth. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=129636225 Elderly patients often experience age-related decline in appetite or swallowing difficulties, making enteral feeding a vital support system. Based on type, the surgical suction instruments market is segmented into retractors, yankauer suction tube, poole suction tube, frazier suction tip, others. The yankauer suction tube accounts for the largest share in the surgical suction instruments market, the bulbous tip design and wide opening allow for efficient suction of blood, fluids, and debris from the surgical field. This improves visibility and reduces the risk of obscuring critical structures. which is expected to drive the segment growth. Based on application, the surgical suction instruments market is segmented into general surgery, neurosurgery, orthopedic surgery, cardiovascular surgery, dental surgery. The general surgery accounts for the largest share in the surgical suction instruments market, Surgical suction instruments play a vital role in various aspects of general surgery, contributing to a clean and efficient operative environment. Suction removes blood, fluids, and debris from the surgical site, allowing the surgeon a clear view of the underlying anatomy. This is crucial for precise dissection, minimizing the risk of unintended injury to vital structures which is expected to drive the market growth. In 2023, North America accounted for the largest share of the surgical suction instruments market, followed by Europe and Asia Pacific. The United States and Canada have well-equipped hospitals and a strong focus on advanced medical care, which supports the adoption of surgical suction instruments, also compared to established markets like North America and Europe, the Asia Pacific region often offers lower labor costs, making it an attractive option for companies seeking to optimize manufacturing expenses. The major players in the surgical suction instruments market include include The prominent players in the medical device contract manufacturing market include include Olympus (Japan), Cardinal Health, Inc. (US), Stryker Corporation (US), Medtronic (Ireland), B. Braun Melsungen AG (Germany), CONMED Corporation (US), BD (US), Steris Plc (Ireland), Teleflex Incorporated (US), Carl Zeiss Meditech AG (Germany), Integra Lifesciences Holdings Corporation (US), KARL STORZ SE & CO. KG (Germany), Indosurgicals Private Limited (India), Applied Medical Technology, Inc. (US), Amsino International, Inc.(US), Surtex Instruments Limited (UK), Bionix LLC.(US), Vactechindia.Com (India), Applied Medical Resources Corporation (US), DTR Medical Ltd (UK), Sklar Surgical Instruments (US), PAJUNK (Germany), Hangzhou Kangji Medical Instrument Co.,Ltd.(China), Romsons (India), Narang Medical Limited.(India). Recent Developments of the Surgical Suction Instruments Industry: In January 2024, Olympus Corporation acquired the Taewoong Medical Co., Ltd., a Korea-based manufacturer of medical devices. This acquisition helps Olympus to strengthen its GI Endo Therapy product portfolio capabilities, contribute to improving patient outcomes through comprehensive solutions, and elevate the standard of care. In May 2023, Stryker acquired the Cerus Endovascular Ltd. (UK), a medical device company engaged in the design and development of neurointerventional devices. Cerus Endovascular’s marked products, helped to expand Stryker’s current portfolio of aneurysm treatment solutions. In September 2022, Cardinal Health, Inc. (US) announced the partnership with Kinaxis (Canada) to enhance the Kinaxis RapidResponse Platform used for supply chain agility and medical product visibility. In July 2022, Medtronic and the American Society for Gastrointestinal Endoscopy expanded the Health Equity Assistance Program for colon cancer screening with support from Amazon Web Services. Completed first installation of donated GI Genius intelligent endoscopy modules.

Innovations and Opportunities in the $503 Million Surgical Suction Instruments Market by 2029 https://www.marketsandmarkets.com/Market-Reports/surgical-suction-instruments-market-129636225.html The global surgical suction instruments market is projected to reach 503 million in 2029 from USD 375 million in 2024, at a CAGR of 6.1% between 2024 and 2029. The rising technological advancemnets and increasing geriatric population is driving the growth of the market. As the global population ages, the number of chronic diseases is increasing which is expected to drive the market growth. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=129636225 Elderly patients often experience age-related decline in appetite or swallowing difficulties, making enteral feeding a vital support system. Based on type, the surgical suction instruments market is segmented into retractors, yankauer suction tube, poole suction tube, frazier suction tip, others. The yankauer suction tube accounts for the largest share in the surgical suction instruments market, the bulbous tip design and wide opening allow for efficient suction of blood, fluids, and debris from the surgical field. This improves visibility and reduces the risk of obscuring critical structures. which is expected to drive the segment growth. Based on application, the surgical suction instruments market is segmented into general surgery, neurosurgery, orthopedic surgery, cardiovascular surgery, dental surgery. The general surgery accounts for the largest share in the surgical suction instruments market, Surgical suction instruments play a vital role in various aspects of general surgery, contributing to a clean and efficient operative environment. Suction removes blood, fluids, and debris from the surgical site, allowing the surgeon a clear view of the underlying anatomy. This is crucial for precise dissection, minimizing the risk of unintended injury to vital structures which is expected to drive the market growth. In 2023, North America accounted for the largest share of the surgical suction instruments market, followed by Europe and Asia Pacific. The United States and Canada have well-equipped hospitals and a strong focus on advanced medical care, which supports the adoption of surgical suction instruments, also compared to established markets like North America and Europe, the Asia Pacific region often offers lower labor costs, making it an attractive option for companies seeking to optimize manufacturing expenses. The major players in the surgical suction instruments market include include The prominent players in the medical device contract manufacturing market include include Olympus (Japan), Cardinal Health, Inc. (US), Stryker Corporation (US), Medtronic (Ireland), B. Braun Melsungen AG (Germany), CONMED Corporation (US), BD (US), Steris Plc (Ireland), Teleflex Incorporated (US), Carl Zeiss Meditech AG (Germany), Integra Lifesciences Holdings Corporation (US), KARL STORZ SE & CO. KG (Germany), Indosurgicals Private Limited (India), Applied Medical Technology, Inc. (US), Amsino International, Inc.(US), Surtex Instruments Limited (UK), Bionix LLC.(US), Vactechindia.Com (India), Applied Medical Resources Corporation (US), DTR Medical Ltd (UK), Sklar Surgical Instruments (US), PAJUNK (Germany), Hangzhou Kangji Medical Instrument Co.,Ltd.(China), Romsons (India), Narang Medical Limited.(India). Recent Developments of the Surgical Suction Instruments Industry: In January 2024, Olympus Corporation acquired the Taewoong Medical Co., Ltd., a Korea-based manufacturer of medical devices. This acquisition helps Olympus to strengthen its GI Endo Therapy product portfolio capabilities, contribute to improving patient outcomes through comprehensive solutions, and elevate the standard of care. In May 2023, Stryker acquired the Cerus Endovascular Ltd. (UK), a medical device company engaged in the design and development of neurointerventional devices. Cerus Endovascular’s marked products, helped to expand Stryker’s current portfolio of aneurysm treatment solutions. In September 2022, Cardinal Health, Inc. (US) announced the partnership with Kinaxis (Canada) to enhance the Kinaxis RapidResponse Platform used for supply chain agility and medical product visibility. In July 2022, Medtronic and the American Society for Gastrointestinal Endoscopy expanded the Health Equity Assistance Program for colon cancer screening with support from Amazon Web Services. Completed first installation of donated GI Genius intelligent endoscopy modules. -

-

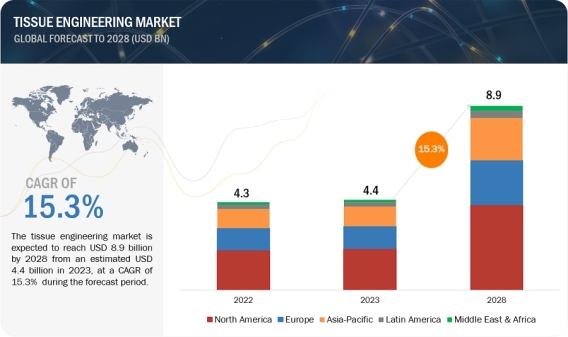

Driving Regenerative Medicine Advances: Tissue Engineering Market to Reach $8.9 Billion by 2028 https://www.marketsandmarkets.com/Market-Reports/tissue-engineering-market-34135173.html The tissue engineering market is expected to reach USD 8.9 billion by 2028 from an estimated USD 4.4 billion in 2023, at a CAGR of 15.3% during the forecast period. The growth is attributed to numerous factors including increasing incidences of road accidents, rising demand for regenerative medicines for the treatment of chronic diseases, and growing technological advancements in the biopharmaceutical sector. In addition, increasing research activities in the field of tissue engineering is promoting the growth of the tissue engineering market. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=34135173 3D bioprinting is an innovative technology in tissue engineering, that enables the precise fabrication of intricate tissue structures, vital for regenerative medicine and drug testing. Its development is primarily propelled by continual technological advancements, including improved bio inks and printing techniques, coupled with the critical need to address organ shortages and revolutionize medical treatments. Material innovation also plays a pivotal role, in fostering the creation of biocompatible substances essential for enhancing the viability and functionality of bio-printed tissues. Additionally, collaborative research efforts among multidisciplinary fields drive progress, promising transformative solutions in healthcare. Based on product type, the tissue engineering market has been segmented into scaffolds, tissue grafts, and other products. In 2022, scaffolds accounted for the largest market share. Scaffold-driven tissue engineering hinges on biocompatibility, mechanical robustness, and optimal pore structure for cell infiltration and nutrient exchange. Integration of bioactive cues and vascular-like properties also fuels advancements, crucial for crafting functional and viable engineered tissues. These driving factors collectively shape scaffold design, influencing their efficacy in tissue engineering applications. Based on material, the global tissue engineering market is segmented into synthetic materials and biologically derived materials. Synthetic material accounted for major market share of the tissue engineering market in 2022. The large share of this segment can be attributed to the cost effectiveness of the synthetic products as compared to the biologically derived products. In addition, increasing demand for advanced and cost-effective tissue engineering solutions is propelling the growth of the synthetic material segment in the tissue engineering market. Based on application, the tissue engineering market is segmented into orthopedics & musculoskeletal disorders, dermatology & wound care, dental disorders, cardiovascular diseases, and others. In 2022, orthopedics & musculoskeletal disorders accounted for the largest share of the global tissue engineering market. The large share of the segment can primarily be attributed to rising demand for high quality tissue engineering products for the repair and reconstruction of damaged tissues or organs. Additionally, increasing incidences of road accidents are promoting the adoption of tissue engineering products for tissue reconstruction. Based on end users, the tissue engineering market has been segmented into hospitals, specialty centers and clinics, and ambulatory surgical centers. Hospitals accounted for the largest market share of the tissue engineering market. The large share of the segment can primarily be attributed to the increasing demand for advanced regeneration solutions for the reconstruction and regeneration of tissues. Additionally, the increasing rate of chronic and degenerative diseases is driving the demand for hospitals. The key regional markets for the global tissue engineering market are Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa. In 2022, North America accounted for the largest share of the market. The large share of this region can be attributed to the growing technological developments in the healthcare sector and rising research activities for the advancements of the tissue engineering field. However, most of the growth in the market is expected from emerging countries across Asia Pacific. During the forecast period, the Asia Pacific is expected to grow with the fastest CAGR due to the increasing adoption of innovative technologies for the treatment of chronic and degenerative diseases. Key players in the global tissue engineering market include Organogenesis (US), AbbVie Inc. (US), Baxter (US), BD (US), B. Braun (Germany), TEIJIN Limited (Japan), Institut Straumann AG (Switzerland), Integra Lifesciences (US), Johnson & Johnson Services, Inc. (US), Medtronic (Ireland), NuVasive, Inc. (US), Stryker (US), Terumo Corporation (Japan), W. L. Gore & Associates Inc. (US), Zimmer Biomet (US), Smith & Nephew plc (UK), MIMEDX Group, Inc. (US), BioTissue (US), CollPlant Biotechnologies Ltd. (Israel), Sumitomo Pharma Co., Ltd. (Japan), Matricel GmbH (Germany), Mallinckrodt (US), Regrow Biosciences Pvt Ltd (India), Vericel Corporation (US), Tecnoss S.R.L. (Italy), Tegoscience (South Korea), and Tissue Regenix (UK). Recent Developments of Tissue Engineering Industry In September 2023, MIMEDX Group Inc. launched EPIEFFECT to broaden its advanced wound care product portfolio. EPIEFFECT is a lyophilized human placental-based allograft consisting of amnion and chorion membranes. In July 2023, Teijin Limited launched SYNFOLIUM, a cardiovascular surgical patch and received manufacturing and marketing approval in Japan. The cardiovascular surgical patch is used for the surgical treatment of congenital heart disease (CHD). In July 2021, Integra Lifesciences introduced SurgiMend, a collagen matrix. The product is used for soft tissue repair and reconstruction. In May 2020, AbbVie Inc. (US) acquired Allergan plc (Ireland) to expand the product portfolio in therapeutics categories. Allergan plc provides new growth opportunities to AbbVie Inc. in neuroscience with Vraylar, Botox therapeutics, and global aesthetics business.

Driving Regenerative Medicine Advances: Tissue Engineering Market to Reach $8.9 Billion by 2028 https://www.marketsandmarkets.com/Market-Reports/tissue-engineering-market-34135173.html The tissue engineering market is expected to reach USD 8.9 billion by 2028 from an estimated USD 4.4 billion in 2023, at a CAGR of 15.3% during the forecast period. The growth is attributed to numerous factors including increasing incidences of road accidents, rising demand for regenerative medicines for the treatment of chronic diseases, and growing technological advancements in the biopharmaceutical sector. In addition, increasing research activities in the field of tissue engineering is promoting the growth of the tissue engineering market. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=34135173 3D bioprinting is an innovative technology in tissue engineering, that enables the precise fabrication of intricate tissue structures, vital for regenerative medicine and drug testing. Its development is primarily propelled by continual technological advancements, including improved bio inks and printing techniques, coupled with the critical need to address organ shortages and revolutionize medical treatments. Material innovation also plays a pivotal role, in fostering the creation of biocompatible substances essential for enhancing the viability and functionality of bio-printed tissues. Additionally, collaborative research efforts among multidisciplinary fields drive progress, promising transformative solutions in healthcare. Based on product type, the tissue engineering market has been segmented into scaffolds, tissue grafts, and other products. In 2022, scaffolds accounted for the largest market share. Scaffold-driven tissue engineering hinges on biocompatibility, mechanical robustness, and optimal pore structure for cell infiltration and nutrient exchange. Integration of bioactive cues and vascular-like properties also fuels advancements, crucial for crafting functional and viable engineered tissues. These driving factors collectively shape scaffold design, influencing their efficacy in tissue engineering applications. Based on material, the global tissue engineering market is segmented into synthetic materials and biologically derived materials. Synthetic material accounted for major market share of the tissue engineering market in 2022. The large share of this segment can be attributed to the cost effectiveness of the synthetic products as compared to the biologically derived products. In addition, increasing demand for advanced and cost-effective tissue engineering solutions is propelling the growth of the synthetic material segment in the tissue engineering market. Based on application, the tissue engineering market is segmented into orthopedics & musculoskeletal disorders, dermatology & wound care, dental disorders, cardiovascular diseases, and others. In 2022, orthopedics & musculoskeletal disorders accounted for the largest share of the global tissue engineering market. The large share of the segment can primarily be attributed to rising demand for high quality tissue engineering products for the repair and reconstruction of damaged tissues or organs. Additionally, increasing incidences of road accidents are promoting the adoption of tissue engineering products for tissue reconstruction. Based on end users, the tissue engineering market has been segmented into hospitals, specialty centers and clinics, and ambulatory surgical centers. Hospitals accounted for the largest market share of the tissue engineering market. The large share of the segment can primarily be attributed to the increasing demand for advanced regeneration solutions for the reconstruction and regeneration of tissues. Additionally, the increasing rate of chronic and degenerative diseases is driving the demand for hospitals. The key regional markets for the global tissue engineering market are Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa. In 2022, North America accounted for the largest share of the market. The large share of this region can be attributed to the growing technological developments in the healthcare sector and rising research activities for the advancements of the tissue engineering field. However, most of the growth in the market is expected from emerging countries across Asia Pacific. During the forecast period, the Asia Pacific is expected to grow with the fastest CAGR due to the increasing adoption of innovative technologies for the treatment of chronic and degenerative diseases. Key players in the global tissue engineering market include Organogenesis (US), AbbVie Inc. (US), Baxter (US), BD (US), B. Braun (Germany), TEIJIN Limited (Japan), Institut Straumann AG (Switzerland), Integra Lifesciences (US), Johnson & Johnson Services, Inc. (US), Medtronic (Ireland), NuVasive, Inc. (US), Stryker (US), Terumo Corporation (Japan), W. L. Gore & Associates Inc. (US), Zimmer Biomet (US), Smith & Nephew plc (UK), MIMEDX Group, Inc. (US), BioTissue (US), CollPlant Biotechnologies Ltd. (Israel), Sumitomo Pharma Co., Ltd. (Japan), Matricel GmbH (Germany), Mallinckrodt (US), Regrow Biosciences Pvt Ltd (India), Vericel Corporation (US), Tecnoss S.R.L. (Italy), Tegoscience (South Korea), and Tissue Regenix (UK). Recent Developments of Tissue Engineering Industry In September 2023, MIMEDX Group Inc. launched EPIEFFECT to broaden its advanced wound care product portfolio. EPIEFFECT is a lyophilized human placental-based allograft consisting of amnion and chorion membranes. In July 2023, Teijin Limited launched SYNFOLIUM, a cardiovascular surgical patch and received manufacturing and marketing approval in Japan. The cardiovascular surgical patch is used for the surgical treatment of congenital heart disease (CHD). In July 2021, Integra Lifesciences introduced SurgiMend, a collagen matrix. The product is used for soft tissue repair and reconstruction. In May 2020, AbbVie Inc. (US) acquired Allergan plc (Ireland) to expand the product portfolio in therapeutics categories. Allergan plc provides new growth opportunities to AbbVie Inc. in neuroscience with Vraylar, Botox therapeutics, and global aesthetics business. -

-

Understanding the $549 Million Base Editing Market: A Deep Dive https://www.marketsandmarkets.com/Market-Reports/base-editing-market-21238371.html The base editing market is projected to reach USD 549 million by 2028 from an estimated USD 270 million in 2023, at a CAGR of 15.2% during the forecast period. Factors like the rising prevalence of genetic diseases, coupled with advancements in molecular biology and biotechnology, has spurred research and development efforts in base editing technologies. Additionally, the growing investment in gene therapy and the biopharmaceutical sector further accelerates the expansion of the base editing market. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=21238371 Based on product & service, the base editing market is segmented into products and services. The product segment is further categorized as platform, kits & reagents, plasmids, and base editing libraries. The service segment is further categorized as gRNA design/synthesis, cell line engineering, and other services. Platform accounted for the largest share of the global base editing market in 2022. The large share of this segment can primarily be attributed to the increasing demand for base editing in molecular studies and the discovery of new therapies. Based on type, the global base editing market is segmented into DNA base editing, and RNA base editing. In 2022, DNA-targeted base editing accounted for the largest share of the base editing market. The large share of this segment can be attributed to the factor that DNA base editing leads to changes in the genomic DNA sequence, making the edits permanent. This can be advantageous when long-lasting or heritable modifications are desired, as the edited DNA is passed on to subsequent generations of cells. Based on targeted base, the base editing market has been segmented into cytosine base editing, and adenine base editing. In 2022, cytosine base editing accounted for the largest market share because cytosine base editors (CBEs) are designed to convert a C-G base pair to a T-A base pair. This type of transition is more common in naturally occurring DNA sequences, making cytosine editing suitable for introducing changes that are biologically relevant. Based on application, the base editing market has been segmented into drug discovery & development, agriculture, and veterinary. In 2022, the drug discovery & development segment accounted for the largest share of the base editing market. The large share of this segment can be attributed to the potential of base editing for developing novel therapeutic interventions by correcting disease-causing mutations at the DNA or RNA level. This is especially relevant for genetic disorders where a single nucleotide mutation is responsible for the disease. Based on end users, the base editing market has been segmented into pharmaceutical & biotechnology companies, academic research institutes, and contract research organizations. In 2022, the pharmaceutical & biotechnology segment accounted for the largest share of the base editing market. The large share of this segment is due to the potential of base editing in drug development; companies in the pharmaceutical and biotechnology sectors are investing in this technology to secure intellectual property, technology, and product rights and gain a competitive advantage in the rapidly evolving field of genome editing. For instance, in October 2023, Beam Therapeutics announced an agreement with Eli Lilly and Company (Lilly) to acquire certain rights under Beam’s collaboration and license agreement with Verve Therapeutics, Inc., including Beam’s opt-in rights to co-develop and co-commercialize Verve’s base editing programs for cardiovascular disease. The key regional markets for the global base editing market are North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2022, North America accounted for the largest share of the market. The large share of this region is due to the robust biotechnology and pharmaceutical industry, with numerous companies dedicated to drug discovery, development, and therapeutic applications. These companies actively invest in and adopt emerging technologies like base editing for advancing their research and product pipelines. However, most of the growth in the market is expected from emerging countries across Asia Pacific. During the forecast period, the Asia Pacific is expected to be the fastest-growing regional market. Factors such as the emergence of CROs for outsourcing drug discovery-related research projects and increasing pharmaceutical drug pipelines are driving growth in these markets. Key players in the global Base editing market include Danaher Corporation (US), Merck KGaA (Germany), Revvity (US), Maravai LifeSciences (US), GenScript (China), Beam Therapeutics (US), Intellia Therapeutics, Inc. (US), Cellectis (France), ElevateBio (US), Creative Biogene (US), Bio Palette Co., Ltd (Japan), Addgene (US), Synthego (US), EdiGene, Inc. (China), Shape TX (US), Pairwise (US), ProQR Therapeutics (Netherlands), QI-Biodesign (China), KromaTiD, Inc. (US), and GenKOre. (South Korea). Recent Developments of Base Editing Industry: In May 2023, Revvity entered into a license agreement with AstraZeneca for the technology underlying its Pin-point base editing system, a next-generation modular gene editing platform with a strong safety profile to support their creation of cell therapies for the treatment of cancer and immune-mediated diseases. In July 2022, Beam Therapeutics entered a collaboration with Verve Therapeutics. Beam Tx granted Verve Tx a license toward an additional liver-mediated cardiovascular disease target. In February 2022, Intellia Therapeutics acquired Rewrite Therapeutics; a private biotechnology company focused on advancing novel DNA writing technologies. This acquisition has expanded Intellia’s industry-leading genome editing toolbox by adding a platform that is highly complementary to its existing CRISPR/Cas9 and base editing technologies.

Understanding the $549 Million Base Editing Market: A Deep Dive https://www.marketsandmarkets.com/Market-Reports/base-editing-market-21238371.html The base editing market is projected to reach USD 549 million by 2028 from an estimated USD 270 million in 2023, at a CAGR of 15.2% during the forecast period. Factors like the rising prevalence of genetic diseases, coupled with advancements in molecular biology and biotechnology, has spurred research and development efforts in base editing technologies. Additionally, the growing investment in gene therapy and the biopharmaceutical sector further accelerates the expansion of the base editing market. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=21238371 Based on product & service, the base editing market is segmented into products and services. The product segment is further categorized as platform, kits & reagents, plasmids, and base editing libraries. The service segment is further categorized as gRNA design/synthesis, cell line engineering, and other services. Platform accounted for the largest share of the global base editing market in 2022. The large share of this segment can primarily be attributed to the increasing demand for base editing in molecular studies and the discovery of new therapies. Based on type, the global base editing market is segmented into DNA base editing, and RNA base editing. In 2022, DNA-targeted base editing accounted for the largest share of the base editing market. The large share of this segment can be attributed to the factor that DNA base editing leads to changes in the genomic DNA sequence, making the edits permanent. This can be advantageous when long-lasting or heritable modifications are desired, as the edited DNA is passed on to subsequent generations of cells. Based on targeted base, the base editing market has been segmented into cytosine base editing, and adenine base editing. In 2022, cytosine base editing accounted for the largest market share because cytosine base editors (CBEs) are designed to convert a C-G base pair to a T-A base pair. This type of transition is more common in naturally occurring DNA sequences, making cytosine editing suitable for introducing changes that are biologically relevant. Based on application, the base editing market has been segmented into drug discovery & development, agriculture, and veterinary. In 2022, the drug discovery & development segment accounted for the largest share of the base editing market. The large share of this segment can be attributed to the potential of base editing for developing novel therapeutic interventions by correcting disease-causing mutations at the DNA or RNA level. This is especially relevant for genetic disorders where a single nucleotide mutation is responsible for the disease. Based on end users, the base editing market has been segmented into pharmaceutical & biotechnology companies, academic research institutes, and contract research organizations. In 2022, the pharmaceutical & biotechnology segment accounted for the largest share of the base editing market. The large share of this segment is due to the potential of base editing in drug development; companies in the pharmaceutical and biotechnology sectors are investing in this technology to secure intellectual property, technology, and product rights and gain a competitive advantage in the rapidly evolving field of genome editing. For instance, in October 2023, Beam Therapeutics announced an agreement with Eli Lilly and Company (Lilly) to acquire certain rights under Beam’s collaboration and license agreement with Verve Therapeutics, Inc., including Beam’s opt-in rights to co-develop and co-commercialize Verve’s base editing programs for cardiovascular disease. The key regional markets for the global base editing market are North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2022, North America accounted for the largest share of the market. The large share of this region is due to the robust biotechnology and pharmaceutical industry, with numerous companies dedicated to drug discovery, development, and therapeutic applications. These companies actively invest in and adopt emerging technologies like base editing for advancing their research and product pipelines. However, most of the growth in the market is expected from emerging countries across Asia Pacific. During the forecast period, the Asia Pacific is expected to be the fastest-growing regional market. Factors such as the emergence of CROs for outsourcing drug discovery-related research projects and increasing pharmaceutical drug pipelines are driving growth in these markets. Key players in the global Base editing market include Danaher Corporation (US), Merck KGaA (Germany), Revvity (US), Maravai LifeSciences (US), GenScript (China), Beam Therapeutics (US), Intellia Therapeutics, Inc. (US), Cellectis (France), ElevateBio (US), Creative Biogene (US), Bio Palette Co., Ltd (Japan), Addgene (US), Synthego (US), EdiGene, Inc. (China), Shape TX (US), Pairwise (US), ProQR Therapeutics (Netherlands), QI-Biodesign (China), KromaTiD, Inc. (US), and GenKOre. (South Korea). Recent Developments of Base Editing Industry: In May 2023, Revvity entered into a license agreement with AstraZeneca for the technology underlying its Pin-point base editing system, a next-generation modular gene editing platform with a strong safety profile to support their creation of cell therapies for the treatment of cancer and immune-mediated diseases. In July 2022, Beam Therapeutics entered a collaboration with Verve Therapeutics. Beam Tx granted Verve Tx a license toward an additional liver-mediated cardiovascular disease target. In February 2022, Intellia Therapeutics acquired Rewrite Therapeutics; a private biotechnology company focused on advancing novel DNA writing technologies. This acquisition has expanded Intellia’s industry-leading genome editing toolbox by adding a platform that is highly complementary to its existing CRISPR/Cas9 and base editing technologies. -

-

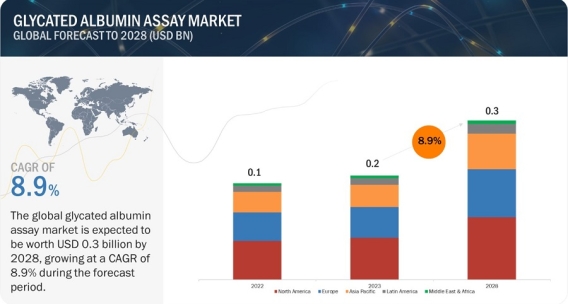

Market Dynamics: Glycated Albumin Assay Expected to Hit $0.3 Billion by 2028 https://www.marketsandmarkets.com/Market-Reports/glycated-albumin-assay-market-265553363.html The global glycated albumin assay market is projected to reach USD 0.3 billion by 2028 from USD 0.2 billion in 2023, at a CAGR of 8.9% during the forecast period. The increased number of diabetes cases is the major factor driving the glycated albumin assay market’s growth. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=265553363 The technologies that power glycated albumin assays are rapidly evolving to help overcome some challenges of utilizing these tests, including improving their clinical utility. The peroxidase method is an example that uses an immunological sandwich amplification and the enzyme peroxidase to affect a signal. This procedure is the enzyme-antibody solution, the PAP immune complex. It is exquisitely sensitive and has been used with high sensitivity and specificity. The glycated albumin assay market is segmented based on application into prediabetes, type 1 diabetes, and type 2 diabetes. In 2022, the type 2 diabetes segment accounted for the largest glycated albumin assay market share. The significant growth of this segment is mainly attributed to the increased burden of type 2 diabetes worldwide, especially in the emerging countries in Asia Pacific, and increased government focus on the diagnosis of diabetes and ailments related to diabetes. Based on end user, the glycated albumin assay market is segmented into hospitals and diabetes care centers, diagnostic laboratories,, and other end users. The hospital and diabetes care centers segment accounted for the largest glycated albumin assay market share in 2022. The increasing number of hospitals worldwide, owing to the growing burden of diseases & disorders, is a primary growth driver for this segment. Major economies are focusing on increasing the establishment of hospitals in their respective healthcare systems. North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa are the five main geographic segments of the worldwide glycated albumin assay market. The North American market is estimated to experience the highest share during the forecast period. The increasing population of elderly (65 years and above) and their age-related chronic diseases and improved focus on spreading awareness of the importance of early diagnosis and control of chronic diseases like diabetes can be credited for North America's significant market share. Asahi Kasei Corporation (Japan), Beijing Strong Biotechnologies, Inc. (China), Diazyme Laboratories, Inc. (US), DxGen Corp. (South Korea), Weldon Biotech, Inc. (India), Hymes Biotech (China) are some of the key players operating in this ecosystem. Several countries in the Asia Pacific region have also implemented initiatives to promote the adoption of early diagnosis of diabetes and related diseases. For instance, countries such as India and Japan have launched precision diabetes diagnosis and control programs focusing on diabetes-related research and diabetes diagnosis and control in routine healthcare. Such factors are expected to support the region's glycated albumin assay market growth. Some key players in the glycated albumin assay market are Asahi Kasei Corporation (Japan), Beijing Strong Biotechnologies, Inc. (China), Diazyme Laboratories, Inc. (US), DxGen Corp. (South Korea), Weldon Biotech, Inc. (India), and Hzymes Biotech (China). The market leadership of these players stems from their comprehensive product portfolios. These dominant market players possess several advantages, including strong marketing and distribution networks, substantial research and development budgets, and well-established brand recognition.

Market Dynamics: Glycated Albumin Assay Expected to Hit $0.3 Billion by 2028 https://www.marketsandmarkets.com/Market-Reports/glycated-albumin-assay-market-265553363.html The global glycated albumin assay market is projected to reach USD 0.3 billion by 2028 from USD 0.2 billion in 2023, at a CAGR of 8.9% during the forecast period. The increased number of diabetes cases is the major factor driving the glycated albumin assay market’s growth. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=265553363 The technologies that power glycated albumin assays are rapidly evolving to help overcome some challenges of utilizing these tests, including improving their clinical utility. The peroxidase method is an example that uses an immunological sandwich amplification and the enzyme peroxidase to affect a signal. This procedure is the enzyme-antibody solution, the PAP immune complex. It is exquisitely sensitive and has been used with high sensitivity and specificity. The glycated albumin assay market is segmented based on application into prediabetes, type 1 diabetes, and type 2 diabetes. In 2022, the type 2 diabetes segment accounted for the largest glycated albumin assay market share. The significant growth of this segment is mainly attributed to the increased burden of type 2 diabetes worldwide, especially in the emerging countries in Asia Pacific, and increased government focus on the diagnosis of diabetes and ailments related to diabetes. Based on end user, the glycated albumin assay market is segmented into hospitals and diabetes care centers, diagnostic laboratories,, and other end users. The hospital and diabetes care centers segment accounted for the largest glycated albumin assay market share in 2022. The increasing number of hospitals worldwide, owing to the growing burden of diseases & disorders, is a primary growth driver for this segment. Major economies are focusing on increasing the establishment of hospitals in their respective healthcare systems. North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa are the five main geographic segments of the worldwide glycated albumin assay market. The North American market is estimated to experience the highest share during the forecast period. The increasing population of elderly (65 years and above) and their age-related chronic diseases and improved focus on spreading awareness of the importance of early diagnosis and control of chronic diseases like diabetes can be credited for North America's significant market share. Asahi Kasei Corporation (Japan), Beijing Strong Biotechnologies, Inc. (China), Diazyme Laboratories, Inc. (US), DxGen Corp. (South Korea), Weldon Biotech, Inc. (India), Hymes Biotech (China) are some of the key players operating in this ecosystem. Several countries in the Asia Pacific region have also implemented initiatives to promote the adoption of early diagnosis of diabetes and related diseases. For instance, countries such as India and Japan have launched precision diabetes diagnosis and control programs focusing on diabetes-related research and diabetes diagnosis and control in routine healthcare. Such factors are expected to support the region's glycated albumin assay market growth. Some key players in the glycated albumin assay market are Asahi Kasei Corporation (Japan), Beijing Strong Biotechnologies, Inc. (China), Diazyme Laboratories, Inc. (US), DxGen Corp. (South Korea), Weldon Biotech, Inc. (India), and Hzymes Biotech (China). The market leadership of these players stems from their comprehensive product portfolios. These dominant market players possess several advantages, including strong marketing and distribution networks, substantial research and development budgets, and well-established brand recognition.

Copyright 2019 © P-tweets Refunds