130 results found | searching for "netherlands"

-

-

The Stobart Air Amsterdam Office stands as an essential hub for travelers flying with one of Europe’s prominent regional airlines. Strategically located in Amsterdam’s central business area, the office is easily accessible by public transport and a short distance from Amsterdam Schiphol Airport. This convenience makes it a preferred choice for passengers seeking in-person assistance for their travel arrangements. Known for its efficiency and professionalism, the Stobart Air Office in Amsterdam offers a wide range of services, including flight bookings, ticket modifications, baggage assistance, travel advisories, and schedule clarifications. Whether you're a business traveler heading to a key European destination or a tourist exploring new cities, the staff ensures that your journey is smooth and stress-free. The team at the Amsterdam office is composed of knowledgeable, multilingual representatives who cater to a diverse clientele. Their commitment to personalized service has earned high praise from passengers who value attention to detail and a human touch in today’s increasingly automated travel industry. The office also assists with group travel arrangements and helps with information related to codeshare flights operated in partnership with major airlines. This makes the Stobart Air Amsterdam Office a comprehensive solution for travelers needing clarity and support beyond just basic ticketing. For passengers who appreciate convenience, professionalism, and a customer-first approach, the Amsterdam Office is a trusted resource. It serves not just as a point of contact but as a bridge between travelers and the wider network of European destinations served by Stobart Air. Visit Us: https://www.airlinesofficesdetails.com/offices/stobart-air-amsterdam-office-in-netherlands/

-

-

Netherlands Medical Device Market in 2031 Netherlands Medical Device Market As we approach 2031, the Netherlands Medical Device Market is set to experience transformative growth. The country's commitment to healthcare excellence and innovation is driving the expansion of its medical device sector. Fore more info:- https://wakelet.com/wake/e78jKfoQ6UOGpkKg8gqeG

-

-

Eligibility Criteria for the Netherlands Study Visa To apply for a Netherlands study visa, applicants generally need: - Acceptance into a recognized Dutch educational institution. - Proof of sufficient financial means for tuition and living expenses. - Health insurance covering their stay in the Netherlands. https://www.y-axis.com/visa/study/netherlands/ [more]

-

-

Netherlands Medical Device Market Forecast 2031: The Netherlands Medical Device Market is set to experience significant growth by 2031, driven by a combination of technological innovation, demographic changes, and strategic investments in healthcare. This forecast explores the key drivers and future prospects that will shape the medical device landscape in the Netherlands over the next decade. Fore more info:- https://mubazmohd.wixsite.com/marketresearch/post/key-trends-shaping-the-netherlands-medical-device-market-by-2031

-

-

SAP ERP Migration Partner Netherlands: https://www.vc-erp.com/sap-s4hana-migration-netherlands.html

-

-

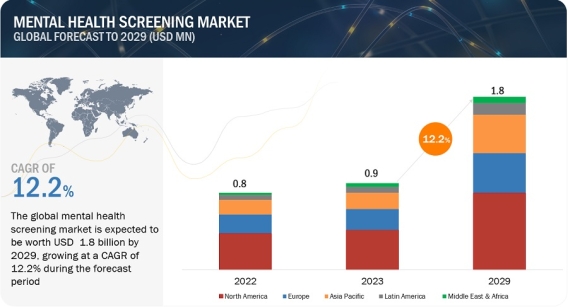

Mental Health Screening Market: Projections and Technological Advances to $1.8 Billion by 2029 https://www.marketsandmarkets.com/Market-Reports/mental-health-screening-market-198516770.html The Mental Health Screening market is projected to reach USD 1.8 billion by 2029 from USD 0.9 billion in 2023, at a CAGR 12.2% during the forecast period 2023-2029. The growth in this market is fuelled by the technological advancements, and the increasing focus on remote monitoring. Furthermore, the integration with wearable technologies and the rise of social media and its impact on the adoption of mental health screening tools, is anticipated to offer lucrative growth opportunities for market players in Mental Health Screening throughout the forecast period 2024-2029. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=198516770 Based on application, the Mental Health Screening market is segmented into physiological, psychiatric, behavioural and cognitive disorders. Physiological disorders are further segmented into depression, anxiety, post-traumatic stress disorder (PTSD), bipolar disorder, eating disorder, substance abuse, and other physiological disorders. Among these sub-segments, substance abuse accounted for the largest share of the Mental Health Screening market in 2023 attributing to the global increase in substance abuse cases, fueled by factors such as stress, trauma, and societal pressures. Growing recognition of the interconnection between mental health and substance abuse play a pivotal role in addressing these challenges by encouraging healthcare providers to adopt integrated screening protocols. Based on technology, the Mental Health Screening market is segmented into self-screening mHealth apps, telehealth & virtual care solutions, continuous monitoring wearable devices, AI-based screening tools, and remote mental health platforms. In 2022, the continuous monitoring wearable devices segment accounted for the largest share attributing to the advancements in wearable sensor technologies and the rising demand for real-time data insights. Based on age group, the Mental Health Screening market is segmented into children & adolescents (age 0–18 years), adults (age 19–64 years), and seniors (age 65 and above). The adults (age 19-64 years) segment accounted for the largest share of the Mental Health Screening market. The rising workloads, economic pressures, and competitive environments contributing to stress and anxiety amplifies the demand for increasing mental health screening solutions among this age group. The Mental Health Screening market is segmented into five major regional segments, namely, North America, Europe, Asia Pacific, Latin America, and Middle East and Africa. In 2022, Asia Pacific was the fastest growing segment in Mental Health Screening market attributed to the growing incidence of mental disorders, rising government initiatives for increasing awareness about mental disorders. Moreover, there is a heightened demand for the improved accessibility of mental health services due to increasing patient burden in this region. Prominent players in Mental health screening market include Proem Behavioral Health (US), SonderMind Inc. (US), Riverside Community Care (US), Headspace Health (US), Quartet Health, Inc. (US), Canary Speech, Inc. (US), Sonde Health, Inc. (US), Koninklijke Philips N.V. (Netherlands), Alphabet Inc. (Fitbit) (US), ResMed (US), Apple Inc. (US), Wellin5 USA Inc. (Canada), Clarigent Health (US), Woebot Labs Inc. (US), Aiberry (US), Cognitive Health Solutions, LLC (US), Adaptive Testing Technologies (US), Thymia Limited (UK), Modern Life, Inc. (US), MoodFit (US), MoodTools (US), Kintsugi Mindful Wellness, Inc. (US), Ellipsis Health Inc. (US), FuturesTHRIVE (US), and CogniABle (India). Recent Development of Mental Health Screening Industry: In November 2023, SonderMind (US) acquired Total Brain (US) to expand its reach, offering individualized mental wellness, supporting therapists with enhanced care techniques, providing population mental health tools for enterprises, and delivering comprehensive solutions to health plans. In October 2023, Ellipsis Health, Inc. (US) partnered with Augmedix (US) to introduce automated mental health screenings during patient visits. In December 2021, Quartet Health, Inc. (US) successfully acquired InnovaTel Telepsychiatry (US), turning its vision of rapidly delivering high-quality mental healthcare for everyone into a reality.

Mental Health Screening Market: Projections and Technological Advances to $1.8 Billion by 2029 https://www.marketsandmarkets.com/Market-Reports/mental-health-screening-market-198516770.html The Mental Health Screening market is projected to reach USD 1.8 billion by 2029 from USD 0.9 billion in 2023, at a CAGR 12.2% during the forecast period 2023-2029. The growth in this market is fuelled by the technological advancements, and the increasing focus on remote monitoring. Furthermore, the integration with wearable technologies and the rise of social media and its impact on the adoption of mental health screening tools, is anticipated to offer lucrative growth opportunities for market players in Mental Health Screening throughout the forecast period 2024-2029. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=198516770 Based on application, the Mental Health Screening market is segmented into physiological, psychiatric, behavioural and cognitive disorders. Physiological disorders are further segmented into depression, anxiety, post-traumatic stress disorder (PTSD), bipolar disorder, eating disorder, substance abuse, and other physiological disorders. Among these sub-segments, substance abuse accounted for the largest share of the Mental Health Screening market in 2023 attributing to the global increase in substance abuse cases, fueled by factors such as stress, trauma, and societal pressures. Growing recognition of the interconnection between mental health and substance abuse play a pivotal role in addressing these challenges by encouraging healthcare providers to adopt integrated screening protocols. Based on technology, the Mental Health Screening market is segmented into self-screening mHealth apps, telehealth & virtual care solutions, continuous monitoring wearable devices, AI-based screening tools, and remote mental health platforms. In 2022, the continuous monitoring wearable devices segment accounted for the largest share attributing to the advancements in wearable sensor technologies and the rising demand for real-time data insights. Based on age group, the Mental Health Screening market is segmented into children & adolescents (age 0–18 years), adults (age 19–64 years), and seniors (age 65 and above). The adults (age 19-64 years) segment accounted for the largest share of the Mental Health Screening market. The rising workloads, economic pressures, and competitive environments contributing to stress and anxiety amplifies the demand for increasing mental health screening solutions among this age group. The Mental Health Screening market is segmented into five major regional segments, namely, North America, Europe, Asia Pacific, Latin America, and Middle East and Africa. In 2022, Asia Pacific was the fastest growing segment in Mental Health Screening market attributed to the growing incidence of mental disorders, rising government initiatives for increasing awareness about mental disorders. Moreover, there is a heightened demand for the improved accessibility of mental health services due to increasing patient burden in this region. Prominent players in Mental health screening market include Proem Behavioral Health (US), SonderMind Inc. (US), Riverside Community Care (US), Headspace Health (US), Quartet Health, Inc. (US), Canary Speech, Inc. (US), Sonde Health, Inc. (US), Koninklijke Philips N.V. (Netherlands), Alphabet Inc. (Fitbit) (US), ResMed (US), Apple Inc. (US), Wellin5 USA Inc. (Canada), Clarigent Health (US), Woebot Labs Inc. (US), Aiberry (US), Cognitive Health Solutions, LLC (US), Adaptive Testing Technologies (US), Thymia Limited (UK), Modern Life, Inc. (US), MoodFit (US), MoodTools (US), Kintsugi Mindful Wellness, Inc. (US), Ellipsis Health Inc. (US), FuturesTHRIVE (US), and CogniABle (India). Recent Development of Mental Health Screening Industry: In November 2023, SonderMind (US) acquired Total Brain (US) to expand its reach, offering individualized mental wellness, supporting therapists with enhanced care techniques, providing population mental health tools for enterprises, and delivering comprehensive solutions to health plans. In October 2023, Ellipsis Health, Inc. (US) partnered with Augmedix (US) to introduce automated mental health screenings during patient visits. In December 2021, Quartet Health, Inc. (US) successfully acquired InnovaTel Telepsychiatry (US), turning its vision of rapidly delivering high-quality mental healthcare for everyone into a reality. -

-

Understanding the $549 Million Base Editing Market: A Deep Dive https://www.marketsandmarkets.com/Market-Reports/base-editing-market-21238371.html The base editing market is projected to reach USD 549 million by 2028 from an estimated USD 270 million in 2023, at a CAGR of 15.2% during the forecast period. Factors like the rising prevalence of genetic diseases, coupled with advancements in molecular biology and biotechnology, has spurred research and development efforts in base editing technologies. Additionally, the growing investment in gene therapy and the biopharmaceutical sector further accelerates the expansion of the base editing market. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=21238371 Based on product & service, the base editing market is segmented into products and services. The product segment is further categorized as platform, kits & reagents, plasmids, and base editing libraries. The service segment is further categorized as gRNA design/synthesis, cell line engineering, and other services. Platform accounted for the largest share of the global base editing market in 2022. The large share of this segment can primarily be attributed to the increasing demand for base editing in molecular studies and the discovery of new therapies. Based on type, the global base editing market is segmented into DNA base editing, and RNA base editing. In 2022, DNA-targeted base editing accounted for the largest share of the base editing market. The large share of this segment can be attributed to the factor that DNA base editing leads to changes in the genomic DNA sequence, making the edits permanent. This can be advantageous when long-lasting or heritable modifications are desired, as the edited DNA is passed on to subsequent generations of cells. Based on targeted base, the base editing market has been segmented into cytosine base editing, and adenine base editing. In 2022, cytosine base editing accounted for the largest market share because cytosine base editors (CBEs) are designed to convert a C-G base pair to a T-A base pair. This type of transition is more common in naturally occurring DNA sequences, making cytosine editing suitable for introducing changes that are biologically relevant. Based on application, the base editing market has been segmented into drug discovery & development, agriculture, and veterinary. In 2022, the drug discovery & development segment accounted for the largest share of the base editing market. The large share of this segment can be attributed to the potential of base editing for developing novel therapeutic interventions by correcting disease-causing mutations at the DNA or RNA level. This is especially relevant for genetic disorders where a single nucleotide mutation is responsible for the disease. Based on end users, the base editing market has been segmented into pharmaceutical & biotechnology companies, academic research institutes, and contract research organizations. In 2022, the pharmaceutical & biotechnology segment accounted for the largest share of the base editing market. The large share of this segment is due to the potential of base editing in drug development; companies in the pharmaceutical and biotechnology sectors are investing in this technology to secure intellectual property, technology, and product rights and gain a competitive advantage in the rapidly evolving field of genome editing. For instance, in October 2023, Beam Therapeutics announced an agreement with Eli Lilly and Company (Lilly) to acquire certain rights under Beam’s collaboration and license agreement with Verve Therapeutics, Inc., including Beam’s opt-in rights to co-develop and co-commercialize Verve’s base editing programs for cardiovascular disease. The key regional markets for the global base editing market are North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2022, North America accounted for the largest share of the market. The large share of this region is due to the robust biotechnology and pharmaceutical industry, with numerous companies dedicated to drug discovery, development, and therapeutic applications. These companies actively invest in and adopt emerging technologies like base editing for advancing their research and product pipelines. However, most of the growth in the market is expected from emerging countries across Asia Pacific. During the forecast period, the Asia Pacific is expected to be the fastest-growing regional market. Factors such as the emergence of CROs for outsourcing drug discovery-related research projects and increasing pharmaceutical drug pipelines are driving growth in these markets. Key players in the global Base editing market include Danaher Corporation (US), Merck KGaA (Germany), Revvity (US), Maravai LifeSciences (US), GenScript (China), Beam Therapeutics (US), Intellia Therapeutics, Inc. (US), Cellectis (France), ElevateBio (US), Creative Biogene (US), Bio Palette Co., Ltd (Japan), Addgene (US), Synthego (US), EdiGene, Inc. (China), Shape TX (US), Pairwise (US), ProQR Therapeutics (Netherlands), QI-Biodesign (China), KromaTiD, Inc. (US), and GenKOre. (South Korea). Recent Developments of Base Editing Industry: In May 2023, Revvity entered into a license agreement with AstraZeneca for the technology underlying its Pin-point base editing system, a next-generation modular gene editing platform with a strong safety profile to support their creation of cell therapies for the treatment of cancer and immune-mediated diseases. In July 2022, Beam Therapeutics entered a collaboration with Verve Therapeutics. Beam Tx granted Verve Tx a license toward an additional liver-mediated cardiovascular disease target. In February 2022, Intellia Therapeutics acquired Rewrite Therapeutics; a private biotechnology company focused on advancing novel DNA writing technologies. This acquisition has expanded Intellia’s industry-leading genome editing toolbox by adding a platform that is highly complementary to its existing CRISPR/Cas9 and base editing technologies.

Understanding the $549 Million Base Editing Market: A Deep Dive https://www.marketsandmarkets.com/Market-Reports/base-editing-market-21238371.html The base editing market is projected to reach USD 549 million by 2028 from an estimated USD 270 million in 2023, at a CAGR of 15.2% during the forecast period. Factors like the rising prevalence of genetic diseases, coupled with advancements in molecular biology and biotechnology, has spurred research and development efforts in base editing technologies. Additionally, the growing investment in gene therapy and the biopharmaceutical sector further accelerates the expansion of the base editing market. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=21238371 Based on product & service, the base editing market is segmented into products and services. The product segment is further categorized as platform, kits & reagents, plasmids, and base editing libraries. The service segment is further categorized as gRNA design/synthesis, cell line engineering, and other services. Platform accounted for the largest share of the global base editing market in 2022. The large share of this segment can primarily be attributed to the increasing demand for base editing in molecular studies and the discovery of new therapies. Based on type, the global base editing market is segmented into DNA base editing, and RNA base editing. In 2022, DNA-targeted base editing accounted for the largest share of the base editing market. The large share of this segment can be attributed to the factor that DNA base editing leads to changes in the genomic DNA sequence, making the edits permanent. This can be advantageous when long-lasting or heritable modifications are desired, as the edited DNA is passed on to subsequent generations of cells. Based on targeted base, the base editing market has been segmented into cytosine base editing, and adenine base editing. In 2022, cytosine base editing accounted for the largest market share because cytosine base editors (CBEs) are designed to convert a C-G base pair to a T-A base pair. This type of transition is more common in naturally occurring DNA sequences, making cytosine editing suitable for introducing changes that are biologically relevant. Based on application, the base editing market has been segmented into drug discovery & development, agriculture, and veterinary. In 2022, the drug discovery & development segment accounted for the largest share of the base editing market. The large share of this segment can be attributed to the potential of base editing for developing novel therapeutic interventions by correcting disease-causing mutations at the DNA or RNA level. This is especially relevant for genetic disorders where a single nucleotide mutation is responsible for the disease. Based on end users, the base editing market has been segmented into pharmaceutical & biotechnology companies, academic research institutes, and contract research organizations. In 2022, the pharmaceutical & biotechnology segment accounted for the largest share of the base editing market. The large share of this segment is due to the potential of base editing in drug development; companies in the pharmaceutical and biotechnology sectors are investing in this technology to secure intellectual property, technology, and product rights and gain a competitive advantage in the rapidly evolving field of genome editing. For instance, in October 2023, Beam Therapeutics announced an agreement with Eli Lilly and Company (Lilly) to acquire certain rights under Beam’s collaboration and license agreement with Verve Therapeutics, Inc., including Beam’s opt-in rights to co-develop and co-commercialize Verve’s base editing programs for cardiovascular disease. The key regional markets for the global base editing market are North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2022, North America accounted for the largest share of the market. The large share of this region is due to the robust biotechnology and pharmaceutical industry, with numerous companies dedicated to drug discovery, development, and therapeutic applications. These companies actively invest in and adopt emerging technologies like base editing for advancing their research and product pipelines. However, most of the growth in the market is expected from emerging countries across Asia Pacific. During the forecast period, the Asia Pacific is expected to be the fastest-growing regional market. Factors such as the emergence of CROs for outsourcing drug discovery-related research projects and increasing pharmaceutical drug pipelines are driving growth in these markets. Key players in the global Base editing market include Danaher Corporation (US), Merck KGaA (Germany), Revvity (US), Maravai LifeSciences (US), GenScript (China), Beam Therapeutics (US), Intellia Therapeutics, Inc. (US), Cellectis (France), ElevateBio (US), Creative Biogene (US), Bio Palette Co., Ltd (Japan), Addgene (US), Synthego (US), EdiGene, Inc. (China), Shape TX (US), Pairwise (US), ProQR Therapeutics (Netherlands), QI-Biodesign (China), KromaTiD, Inc. (US), and GenKOre. (South Korea). Recent Developments of Base Editing Industry: In May 2023, Revvity entered into a license agreement with AstraZeneca for the technology underlying its Pin-point base editing system, a next-generation modular gene editing platform with a strong safety profile to support their creation of cell therapies for the treatment of cancer and immune-mediated diseases. In July 2022, Beam Therapeutics entered a collaboration with Verve Therapeutics. Beam Tx granted Verve Tx a license toward an additional liver-mediated cardiovascular disease target. In February 2022, Intellia Therapeutics acquired Rewrite Therapeutics; a private biotechnology company focused on advancing novel DNA writing technologies. This acquisition has expanded Intellia’s industry-leading genome editing toolbox by adding a platform that is highly complementary to its existing CRISPR/Cas9 and base editing technologies. -

-

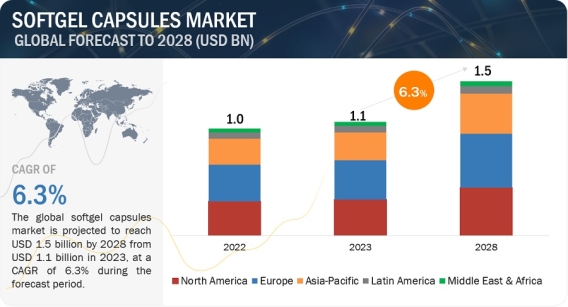

Global Softgel Capsules Market Worth $1.5 Billion by 2028: Key Insights and Analysis https://www.marketsandmarkets.com/Market-Reports/softgel-capsules-market-238329912.html The global softgel capsules market is projected to reach USD 1.5 billion by 2028 from USD 1.1 billion in 2023, at a CAGR of 6.3% during the forecast period. Factors such as advantages of softgel capsules, growing demand for nutraceuticals and dietary supplements, and growing demand for naturally sourced ingredients.However, restricted acceptance due to cultural restrictions is expected to hinder the growth of this market. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=238329912 On the basis of material type, the global softgel market is divided into gelatin, and other materials (such as carrageenan, hydroxypropyl methylcellulose (HPMC), pullulan, and starch-glycerin. In 2022, the gelatin segment accounted for the largest market share. Factors such as the advantages of soft gelatin capsules, such as no taste, unit dose delivery, easy to swallow, tamper-proof, and availability in a wide range of shapes, colors, and sizes, and growing demand for health supplements are supporting the growth of this market. In extension to this the growth of raw materials used for softgel capsules. On the basis of source, the global softgel capsules market has been divided into porcine, bovine, and other sources (including poultry, marine, and plant sources). In 2022, bovine segment accounted for the largest share of softgel capsules market. Bovine softgels are known for their soft and flexible texture, which make them easy to swallow and digest and the abundance and easy availability of bovine are supporting its growth in the market. Strong emphasis on the launch of new products in the market specifically for softgels is further likely to have a positive impact on the market growth. On the basis of application, the global softgel capsules market is divided into pharmaceutical, nutraceutical and dietary supplement, and cosmetics & personal care industries. In 2022, nutraceutical and dietary supplement industry segment accounted for the largest market share. Factors such as the icreasing consumer preference for capsule-based nutraceutical formulations is one of the major factors driving the growth of softgel capsules market for the nutraceutical industry. In addition, the growing demand for specialized dietary supplements is driving innovation in the softgel capsules market. On the basis of region, the softgel capsules market has been segmented into, North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2022, Europe accounted for the largest share of the softgel capsules market followed by North America. Factors such as changes in consumer lifestyles, growth in pharmaceutical industry and the presence of major capsule manufacturers and pharmaceutical giants in the region, such as Gelita AG (Germany), PB Leiner (Belgium), Weishardt SA (France), and Lapi Gelatine S.p.a. (Italy). This is expected to support the growth of softgel capsules market. Key players in the softgel capsules market are Gelita AG (Germany), PB Leiner (part of Tessenderlo Group) (Belgium), Nitta Gelatin, Inc. (Japan), Sterling Gelatin and Croda Colloids (India), Narmada Gelatines Limited (India), Italgel S.r.l. (Italy), Darling Ingredients Inc. (US), Lapi Gelatine S.p.a. (Italy), Trobas Gelatine B.V. (Netherlands), Weishardt (France), India Gelatine & Chemicals Ltd. (India), Xiamen Gelken Gelatin Co., Ltd. (China), Gelco International (Brazil), Boom Gelatin (China), Geliko LLC (US), Kenney & Ross Limited Marine Gelatin (Canada), Baotou Dongbao Bio-Tech Co., Ltd. (China), Jellice Gelatin & Collagen (Netherlands), Athos Collagen Pvt. Ltd. (India), Kubon Biotechnology Co., Ltd. (Cambodia), C.J. Gelatine Products Limited (India), American Gelatin (US), and Geltech (South Korea). Recent Developments of Softgel Capsules Industry In March 2023, Darlings Ingredients Inc. acquired Gelnex, which is a global producer of gelatin and collagen products. This acquisition would give the company the capacity to serve the growing needs of its collagen customers while continuing to serve the growing gelatin market.Thermo fisher launched Tumoroid Culture Medium to accelerate development of novel cancer therapies. In November 2022, PB Leiner established a joint venture with D&D Participações Societárias. Under the terms of this joint venture, D&D Participações Societárias will acquire a minority stake in the shares of the Brazilian plant of PB Leiner (PB Brasil Industria e Comercio de Gelatinas Ltda). The combined strength of the two companies will enable a long-term sustainable offering of a premium product range of beef hide gelatin based on PB Leiner’s technology. In October 2022, PB Leiner extended the gelwoRx Dsolve pharmaceutical portfolio with the launch of three new products—Dsolve B, Dsolve P, and Dsolve xTRA. Dsolve P (pig skin) and Dsolve B (beef hide) are specially developed to reduce cross-linking and fast dissolution of soft capsules. Dsolve xTRA (bovine bone) promises to perform better than Dsolve, Dsolve P, and Dsolve B.

Global Softgel Capsules Market Worth $1.5 Billion by 2028: Key Insights and Analysis https://www.marketsandmarkets.com/Market-Reports/softgel-capsules-market-238329912.html The global softgel capsules market is projected to reach USD 1.5 billion by 2028 from USD 1.1 billion in 2023, at a CAGR of 6.3% during the forecast period. Factors such as advantages of softgel capsules, growing demand for nutraceuticals and dietary supplements, and growing demand for naturally sourced ingredients.However, restricted acceptance due to cultural restrictions is expected to hinder the growth of this market. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=238329912 On the basis of material type, the global softgel market is divided into gelatin, and other materials (such as carrageenan, hydroxypropyl methylcellulose (HPMC), pullulan, and starch-glycerin. In 2022, the gelatin segment accounted for the largest market share. Factors such as the advantages of soft gelatin capsules, such as no taste, unit dose delivery, easy to swallow, tamper-proof, and availability in a wide range of shapes, colors, and sizes, and growing demand for health supplements are supporting the growth of this market. In extension to this the growth of raw materials used for softgel capsules. On the basis of source, the global softgel capsules market has been divided into porcine, bovine, and other sources (including poultry, marine, and plant sources). In 2022, bovine segment accounted for the largest share of softgel capsules market. Bovine softgels are known for their soft and flexible texture, which make them easy to swallow and digest and the abundance and easy availability of bovine are supporting its growth in the market. Strong emphasis on the launch of new products in the market specifically for softgels is further likely to have a positive impact on the market growth. On the basis of application, the global softgel capsules market is divided into pharmaceutical, nutraceutical and dietary supplement, and cosmetics & personal care industries. In 2022, nutraceutical and dietary supplement industry segment accounted for the largest market share. Factors such as the icreasing consumer preference for capsule-based nutraceutical formulations is one of the major factors driving the growth of softgel capsules market for the nutraceutical industry. In addition, the growing demand for specialized dietary supplements is driving innovation in the softgel capsules market. On the basis of region, the softgel capsules market has been segmented into, North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2022, Europe accounted for the largest share of the softgel capsules market followed by North America. Factors such as changes in consumer lifestyles, growth in pharmaceutical industry and the presence of major capsule manufacturers and pharmaceutical giants in the region, such as Gelita AG (Germany), PB Leiner (Belgium), Weishardt SA (France), and Lapi Gelatine S.p.a. (Italy). This is expected to support the growth of softgel capsules market. Key players in the softgel capsules market are Gelita AG (Germany), PB Leiner (part of Tessenderlo Group) (Belgium), Nitta Gelatin, Inc. (Japan), Sterling Gelatin and Croda Colloids (India), Narmada Gelatines Limited (India), Italgel S.r.l. (Italy), Darling Ingredients Inc. (US), Lapi Gelatine S.p.a. (Italy), Trobas Gelatine B.V. (Netherlands), Weishardt (France), India Gelatine & Chemicals Ltd. (India), Xiamen Gelken Gelatin Co., Ltd. (China), Gelco International (Brazil), Boom Gelatin (China), Geliko LLC (US), Kenney & Ross Limited Marine Gelatin (Canada), Baotou Dongbao Bio-Tech Co., Ltd. (China), Jellice Gelatin & Collagen (Netherlands), Athos Collagen Pvt. Ltd. (India), Kubon Biotechnology Co., Ltd. (Cambodia), C.J. Gelatine Products Limited (India), American Gelatin (US), and Geltech (South Korea). Recent Developments of Softgel Capsules Industry In March 2023, Darlings Ingredients Inc. acquired Gelnex, which is a global producer of gelatin and collagen products. This acquisition would give the company the capacity to serve the growing needs of its collagen customers while continuing to serve the growing gelatin market.Thermo fisher launched Tumoroid Culture Medium to accelerate development of novel cancer therapies. In November 2022, PB Leiner established a joint venture with D&D Participações Societárias. Under the terms of this joint venture, D&D Participações Societárias will acquire a minority stake in the shares of the Brazilian plant of PB Leiner (PB Brasil Industria e Comercio de Gelatinas Ltda). The combined strength of the two companies will enable a long-term sustainable offering of a premium product range of beef hide gelatin based on PB Leiner’s technology. In October 2022, PB Leiner extended the gelwoRx Dsolve pharmaceutical portfolio with the launch of three new products—Dsolve B, Dsolve P, and Dsolve xTRA. Dsolve P (pig skin) and Dsolve B (beef hide) are specially developed to reduce cross-linking and fast dissolution of soft capsules. Dsolve xTRA (bovine bone) promises to perform better than Dsolve, Dsolve P, and Dsolve B. -

-

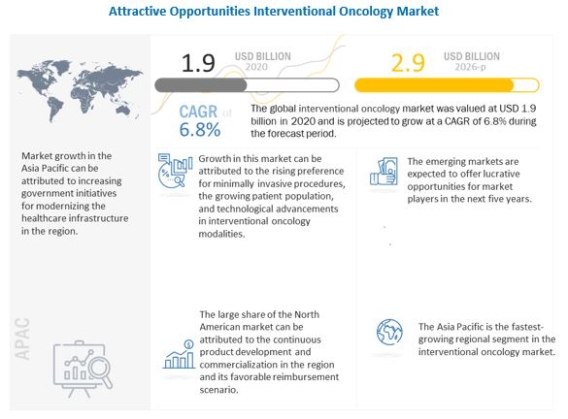

Global Interventional Oncology Market Worth $2.9 Billion by 2026: Key Insights and Analysis https://www.marketsandmarkets.com/Market-Reports/interventional-oncology-market-203687164.html The global interventional oncology market size is expected to grow from USD 1.9 billion in 2020 to USD 2.9 billion in 2026, at a CAGR of 6.8% during the forecast period. Technological advancements in the market are propelling the growth of the interventional oncology market. Additionally, rising incidence of infectious diseases, and increased funding and public-private investments are some of the key factors driving the growth of the interventional oncology market. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=203687164 Based on product, the interventional oncology market is segmented into ablation devices, embolization devices, and support devices. The embolization devices segment accounted for the largest share of 63.8% of the interventional oncology market in 2020. The large share of this segment can be attributed to the rising prevalence of cancer, product enhancements, and the increasing adoption of Yttrium-90 radioembolic agents in emerging countries. Ongoing technological advancements in the field of oncology, rising prevalence of cancer, high healthcare expenditure, are the major factors supporting market growth. Based on procedure, the interventional oncology market is segmented into thermal tumor ablation, non-thermal tumor ablation, transcatheter arterial chemoembolization (TACE), transcatheter arterial radioembolization (TARE) or selective internal radiation therapy (SIRT), and transcatheter arterial embolization (TAE) or bland embolization. In 2020, the TARE/SIRT procedures segment accounted for the largest market share, mainly due to the rising prevalence of cancer, increasing demand for minimally invasive procedures, growing adoption of embolization procedures, and the clinical efficacy of Yttrium-90 radioembolic agents (which are used in these procedures). Based on cancer type, the interventional oncology market is segmented into liver cancer, kidney cancer, lung cancer, bone cancer, and other cancers (includes pediatric cancer, prostate cancer, and breast cancer). The liver cancer segment accounted for the largest share of 63.8% of the interventional oncology market in 2020. The large share of this segment can be attributed to factors such as rising cases of liver cancer across the globe and growing initiatives/research activities for developing advanced liver cancer therapies using interventional oncology. Based on end users, the interventional oncology market is segmented into hospitals, ambulatory surgery centers, and research & academic institutes. Hospitals accounted for the largest share of the market in 2020. The large share of this end-user segment can be attributed to the presence of advanced ICUs & emergency wards in hospitals and the increasing number of surgical procedures performed in hospitals. The interventional oncology market is segmented into five major regions, namely, North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2020, North America was the largest regional market for interventional oncology, with a share of 43.2%. Factors such as continuous development and commercialization of novel interventional oncology products and favorable reimbursements & insurance coverage drive the market for interventional oncology in North America. The Asia Pacific is estimated to be the fastest-growing regional market for interventional oncology. This is due to the rising patient population increasing GDP and healthcare expenditure and growing public awareness about various surgical treatments. Major Players: Medtronic (Ireland), Boston Scientific (US), BD (US), Terumo (Japan), Merit Medical (US), AngioDynamics (US), J&J (US), Teleflex (US), Cook Medical (US), HealthTronics (US), MedWaves (US), Sanarus (US), IMBiotechnologies (Canada), Trod Medical (US), IceCure Medical (Israel), Mermaid Medicals (Denmark), Interface Biomaterials BV (Netherlands), Guerbet (France), ABK Biomedical (Canada), Shape Memory Medical (US), Endo Shape (US), Monteris Medical (US), Instylla (US), Trisalus Lifesciences (US), Profound Medical Corp (Canada), Sirtex (US), Accuray (US), Baylis Medical (Canada), and ALPINION MEDICAL SYSTEMS (South Korea). Recent Developments In 2021, Boston Scientific (US) launched Launched the TheraSphere Y-90 Glass Microspheres In 2018, Merit Medical Systems (US) launched the Preclude IDeal Hydrophilic Sheath Introducer in EMEA markets In 2018, IMBiotechnologies (US) launched ‘Ekobi 500 Embolization Microspheres’ with an enhanced feature of detectability using ultrasound technology. In 2018, Medical City and distributor Gulf Medical Company to install the first IMRIS Surgical Theatre in Saudi Arabia. In 2018, Medtronic (Ireland) launched its OptiSphere embolization spheres designed for hypervascular tumor embolization in the US

Global Interventional Oncology Market Worth $2.9 Billion by 2026: Key Insights and Analysis https://www.marketsandmarkets.com/Market-Reports/interventional-oncology-market-203687164.html The global interventional oncology market size is expected to grow from USD 1.9 billion in 2020 to USD 2.9 billion in 2026, at a CAGR of 6.8% during the forecast period. Technological advancements in the market are propelling the growth of the interventional oncology market. Additionally, rising incidence of infectious diseases, and increased funding and public-private investments are some of the key factors driving the growth of the interventional oncology market. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=203687164 Based on product, the interventional oncology market is segmented into ablation devices, embolization devices, and support devices. The embolization devices segment accounted for the largest share of 63.8% of the interventional oncology market in 2020. The large share of this segment can be attributed to the rising prevalence of cancer, product enhancements, and the increasing adoption of Yttrium-90 radioembolic agents in emerging countries. Ongoing technological advancements in the field of oncology, rising prevalence of cancer, high healthcare expenditure, are the major factors supporting market growth. Based on procedure, the interventional oncology market is segmented into thermal tumor ablation, non-thermal tumor ablation, transcatheter arterial chemoembolization (TACE), transcatheter arterial radioembolization (TARE) or selective internal radiation therapy (SIRT), and transcatheter arterial embolization (TAE) or bland embolization. In 2020, the TARE/SIRT procedures segment accounted for the largest market share, mainly due to the rising prevalence of cancer, increasing demand for minimally invasive procedures, growing adoption of embolization procedures, and the clinical efficacy of Yttrium-90 radioembolic agents (which are used in these procedures). Based on cancer type, the interventional oncology market is segmented into liver cancer, kidney cancer, lung cancer, bone cancer, and other cancers (includes pediatric cancer, prostate cancer, and breast cancer). The liver cancer segment accounted for the largest share of 63.8% of the interventional oncology market in 2020. The large share of this segment can be attributed to factors such as rising cases of liver cancer across the globe and growing initiatives/research activities for developing advanced liver cancer therapies using interventional oncology. Based on end users, the interventional oncology market is segmented into hospitals, ambulatory surgery centers, and research & academic institutes. Hospitals accounted for the largest share of the market in 2020. The large share of this end-user segment can be attributed to the presence of advanced ICUs & emergency wards in hospitals and the increasing number of surgical procedures performed in hospitals. The interventional oncology market is segmented into five major regions, namely, North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2020, North America was the largest regional market for interventional oncology, with a share of 43.2%. Factors such as continuous development and commercialization of novel interventional oncology products and favorable reimbursements & insurance coverage drive the market for interventional oncology in North America. The Asia Pacific is estimated to be the fastest-growing regional market for interventional oncology. This is due to the rising patient population increasing GDP and healthcare expenditure and growing public awareness about various surgical treatments. Major Players: Medtronic (Ireland), Boston Scientific (US), BD (US), Terumo (Japan), Merit Medical (US), AngioDynamics (US), J&J (US), Teleflex (US), Cook Medical (US), HealthTronics (US), MedWaves (US), Sanarus (US), IMBiotechnologies (Canada), Trod Medical (US), IceCure Medical (Israel), Mermaid Medicals (Denmark), Interface Biomaterials BV (Netherlands), Guerbet (France), ABK Biomedical (Canada), Shape Memory Medical (US), Endo Shape (US), Monteris Medical (US), Instylla (US), Trisalus Lifesciences (US), Profound Medical Corp (Canada), Sirtex (US), Accuray (US), Baylis Medical (Canada), and ALPINION MEDICAL SYSTEMS (South Korea). Recent Developments In 2021, Boston Scientific (US) launched Launched the TheraSphere Y-90 Glass Microspheres In 2018, Merit Medical Systems (US) launched the Preclude IDeal Hydrophilic Sheath Introducer in EMEA markets In 2018, IMBiotechnologies (US) launched ‘Ekobi 500 Embolization Microspheres’ with an enhanced feature of detectability using ultrasound technology. In 2018, Medical City and distributor Gulf Medical Company to install the first IMRIS Surgical Theatre in Saudi Arabia. In 2018, Medtronic (Ireland) launched its OptiSphere embolization spheres designed for hypervascular tumor embolization in the US -

-

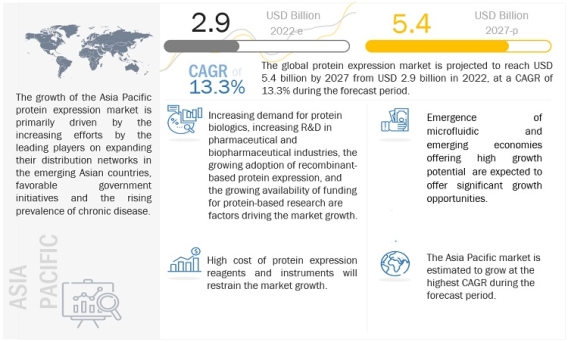

Unlocking the Potential of the $5.4 Billion Protein Expression Market https://www.marketsandmarkets.com/Market-Reports/protein-expression-market-180323924.html According to the new market research report "Protein Expression Market by Type (E.Coli, Mammalian, CHO, HEK 293, Insect, Pichia, Cell-free), Products (Reagents, Vectors, Competent Cells, Instruments, Service), Application (Therapeutic, Industrial), End User, and Region - Global Forecast to 2027", The global protein expression market is expected to reach USD 5.4 billion in 2027 from USD 2.9 billion in 2022 at a CAGR of 13.3% during the forecast period. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=180323924 Factors such as growing pharmaceutical and biotechnology industries, rising adoption of recombinant-based protein expression as well as increasing public and private support through initiatives and funding are favouring the growth of this market. However, the high cost of protein expression reagents and instruments is likely to restrain the growth of this market. Based on system type, the protein expression market is segmented into mammalian cell expression systems, prokaryotic expression systems, insect cell expression systems, yeast expression systems, cell-free expression systems, and algal-based expression systems. The mammalian cell expression systems segment accounted for the largest share of the global protein expression market in 2021. Based on application, the protein expression market is segmented into therapeutic, research and industrial applications. In 2021, the therapeutic applications segment accounted for the largest share of the global protein expression market. Factors such as an increase in protein-based research and the rising prevalence of chronic diseases across the globe contribute to the large share of this market. Based on product & service, the protein expression market is segmented into reagents, expression vectors, competent cells, instruments, and services. The reagents segment accounted for the largest share of the global protein expression market in 2021. Factors such as the increasing research activities in the field of protein expression as well as the large-scale production of antibodies and vaccines are responsible for large share of this market. Based on end users, the protein expression market is segmented into pharmaceutical and biotechnology companies, contract research organizations and contract development and manufacturing organizations (CROs and CDMOs), academic research institutes, and other end users. In 2021, the pharmaceutical and biotechnology companies segment accounted for the largest share of the global protein expression market due to an increase in protein research to understand biological systems and the rising production of recombinant therapeutic proteins for disease treatment. Geographical Growth Scenario: Based on region, the protein expression market is segmented into North America, Europe, Asia Pacific, Rest of the world (Latin America, and the Middle East & Africa). In 2021, North America accounted for the largest share of the global protein expression market, followed by Europe. Factors such as growth in the biotechnology and pharmaceutical industries, the rising prevalence of chronic disorders, and an increase in protein-based therapeutics research investments in the region contribute to its large share. The APAC market is projected to grow at the highest CAGR during the forecast period. Key Players: Thermo Fisher Scientific, Inc (US), Merck KGaA (Germany), GenScript Biotech Corporation (US), Agilent Technologies, Inc. (US), Takara Bio, Inc. (Japan), Bio-Rad Laboratories, Inc. (US), Qiagen N.V (Netherlands), Charles River Laboratories, Inc. (US), Danaher Corporation (US), Sartorius AG (Germany), Corning Incorporated (US), FUJIFILM Irvine Scientific, Inc. (Japan), Lonza Group AG (Switzerland), Bioneer Corporation (South Korea), Promega Corporation (US), Oxford Expression Technologies Ltd. (UK), ProteoGenix (France), Abeomics, Inc. (US), New England Biolabs, Inc. (US), Promab Biotechnologies (US), Sino Biological, Inc. (China), Jena Bioscience (Germany), Lifesensors, Inc. (US), Leading biology, Inc. (US), and Peak Proteins (UK). Recent Developments: In June 2021, Thermo Fisher Scientific Inc. (US) and Advanced Electrophoresis Solutions Ltd. (AES) (Canada) signed an agreement to combine essential protein separation techniques with mass spectrometry (MS) to advance therapeutic protein development through streamlined characterization. In June 2020, Lonza Group AG (Switzerland) launched GSv9, a chemically defined media and feeds platform specifically developed to enhance the performance of the GS Gene Expression System for optimized recombinant protein production.

Unlocking the Potential of the $5.4 Billion Protein Expression Market https://www.marketsandmarkets.com/Market-Reports/protein-expression-market-180323924.html According to the new market research report "Protein Expression Market by Type (E.Coli, Mammalian, CHO, HEK 293, Insect, Pichia, Cell-free), Products (Reagents, Vectors, Competent Cells, Instruments, Service), Application (Therapeutic, Industrial), End User, and Region - Global Forecast to 2027", The global protein expression market is expected to reach USD 5.4 billion in 2027 from USD 2.9 billion in 2022 at a CAGR of 13.3% during the forecast period. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=180323924 Factors such as growing pharmaceutical and biotechnology industries, rising adoption of recombinant-based protein expression as well as increasing public and private support through initiatives and funding are favouring the growth of this market. However, the high cost of protein expression reagents and instruments is likely to restrain the growth of this market. Based on system type, the protein expression market is segmented into mammalian cell expression systems, prokaryotic expression systems, insect cell expression systems, yeast expression systems, cell-free expression systems, and algal-based expression systems. The mammalian cell expression systems segment accounted for the largest share of the global protein expression market in 2021. Based on application, the protein expression market is segmented into therapeutic, research and industrial applications. In 2021, the therapeutic applications segment accounted for the largest share of the global protein expression market. Factors such as an increase in protein-based research and the rising prevalence of chronic diseases across the globe contribute to the large share of this market. Based on product & service, the protein expression market is segmented into reagents, expression vectors, competent cells, instruments, and services. The reagents segment accounted for the largest share of the global protein expression market in 2021. Factors such as the increasing research activities in the field of protein expression as well as the large-scale production of antibodies and vaccines are responsible for large share of this market. Based on end users, the protein expression market is segmented into pharmaceutical and biotechnology companies, contract research organizations and contract development and manufacturing organizations (CROs and CDMOs), academic research institutes, and other end users. In 2021, the pharmaceutical and biotechnology companies segment accounted for the largest share of the global protein expression market due to an increase in protein research to understand biological systems and the rising production of recombinant therapeutic proteins for disease treatment. Geographical Growth Scenario: Based on region, the protein expression market is segmented into North America, Europe, Asia Pacific, Rest of the world (Latin America, and the Middle East & Africa). In 2021, North America accounted for the largest share of the global protein expression market, followed by Europe. Factors such as growth in the biotechnology and pharmaceutical industries, the rising prevalence of chronic disorders, and an increase in protein-based therapeutics research investments in the region contribute to its large share. The APAC market is projected to grow at the highest CAGR during the forecast period. Key Players: Thermo Fisher Scientific, Inc (US), Merck KGaA (Germany), GenScript Biotech Corporation (US), Agilent Technologies, Inc. (US), Takara Bio, Inc. (Japan), Bio-Rad Laboratories, Inc. (US), Qiagen N.V (Netherlands), Charles River Laboratories, Inc. (US), Danaher Corporation (US), Sartorius AG (Germany), Corning Incorporated (US), FUJIFILM Irvine Scientific, Inc. (Japan), Lonza Group AG (Switzerland), Bioneer Corporation (South Korea), Promega Corporation (US), Oxford Expression Technologies Ltd. (UK), ProteoGenix (France), Abeomics, Inc. (US), New England Biolabs, Inc. (US), Promab Biotechnologies (US), Sino Biological, Inc. (China), Jena Bioscience (Germany), Lifesensors, Inc. (US), Leading biology, Inc. (US), and Peak Proteins (UK). Recent Developments: In June 2021, Thermo Fisher Scientific Inc. (US) and Advanced Electrophoresis Solutions Ltd. (AES) (Canada) signed an agreement to combine essential protein separation techniques with mass spectrometry (MS) to advance therapeutic protein development through streamlined characterization. In June 2020, Lonza Group AG (Switzerland) launched GSv9, a chemically defined media and feeds platform specifically developed to enhance the performance of the GS Gene Expression System for optimized recombinant protein production.

Copyright 2019 © P-tweets Refunds