15 results found | searching for "Braun"

-

-

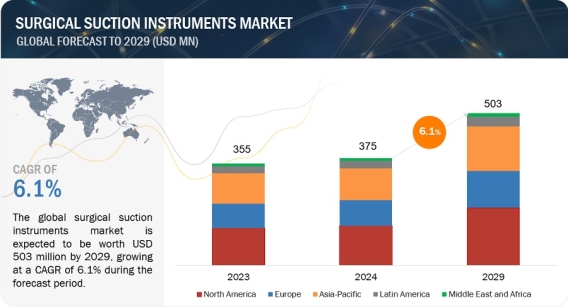

Innovations and Opportunities in the $503 Million Surgical Suction Instruments Market by 2029 https://www.marketsandmarkets.com/Market-Reports/surgical-suction-instruments-market-129636225.html The global surgical suction instruments market is projected to reach 503 million in 2029 from USD 375 million in 2024, at a CAGR of 6.1% between 2024 and 2029. The rising technological advancemnets and increasing geriatric population is driving the growth of the market. As the global population ages, the number of chronic diseases is increasing which is expected to drive the market growth. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=129636225 Elderly patients often experience age-related decline in appetite or swallowing difficulties, making enteral feeding a vital support system. Based on type, the surgical suction instruments market is segmented into retractors, yankauer suction tube, poole suction tube, frazier suction tip, others. The yankauer suction tube accounts for the largest share in the surgical suction instruments market, the bulbous tip design and wide opening allow for efficient suction of blood, fluids, and debris from the surgical field. This improves visibility and reduces the risk of obscuring critical structures. which is expected to drive the segment growth. Based on application, the surgical suction instruments market is segmented into general surgery, neurosurgery, orthopedic surgery, cardiovascular surgery, dental surgery. The general surgery accounts for the largest share in the surgical suction instruments market, Surgical suction instruments play a vital role in various aspects of general surgery, contributing to a clean and efficient operative environment. Suction removes blood, fluids, and debris from the surgical site, allowing the surgeon a clear view of the underlying anatomy. This is crucial for precise dissection, minimizing the risk of unintended injury to vital structures which is expected to drive the market growth. In 2023, North America accounted for the largest share of the surgical suction instruments market, followed by Europe and Asia Pacific. The United States and Canada have well-equipped hospitals and a strong focus on advanced medical care, which supports the adoption of surgical suction instruments, also compared to established markets like North America and Europe, the Asia Pacific region often offers lower labor costs, making it an attractive option for companies seeking to optimize manufacturing expenses. The major players in the surgical suction instruments market include include The prominent players in the medical device contract manufacturing market include include Olympus (Japan), Cardinal Health, Inc. (US), Stryker Corporation (US), Medtronic (Ireland), B. Braun Melsungen AG (Germany), CONMED Corporation (US), BD (US), Steris Plc (Ireland), Teleflex Incorporated (US), Carl Zeiss Meditech AG (Germany), Integra Lifesciences Holdings Corporation (US), KARL STORZ SE & CO. KG (Germany), Indosurgicals Private Limited (India), Applied Medical Technology, Inc. (US), Amsino International, Inc.(US), Surtex Instruments Limited (UK), Bionix LLC.(US), Vactechindia.Com (India), Applied Medical Resources Corporation (US), DTR Medical Ltd (UK), Sklar Surgical Instruments (US), PAJUNK (Germany), Hangzhou Kangji Medical Instrument Co.,Ltd.(China), Romsons (India), Narang Medical Limited.(India). Recent Developments of the Surgical Suction Instruments Industry: In January 2024, Olympus Corporation acquired the Taewoong Medical Co., Ltd., a Korea-based manufacturer of medical devices. This acquisition helps Olympus to strengthen its GI Endo Therapy product portfolio capabilities, contribute to improving patient outcomes through comprehensive solutions, and elevate the standard of care. In May 2023, Stryker acquired the Cerus Endovascular Ltd. (UK), a medical device company engaged in the design and development of neurointerventional devices. Cerus Endovascular’s marked products, helped to expand Stryker’s current portfolio of aneurysm treatment solutions. In September 2022, Cardinal Health, Inc. (US) announced the partnership with Kinaxis (Canada) to enhance the Kinaxis RapidResponse Platform used for supply chain agility and medical product visibility. In July 2022, Medtronic and the American Society for Gastrointestinal Endoscopy expanded the Health Equity Assistance Program for colon cancer screening with support from Amazon Web Services. Completed first installation of donated GI Genius intelligent endoscopy modules.

Innovations and Opportunities in the $503 Million Surgical Suction Instruments Market by 2029 https://www.marketsandmarkets.com/Market-Reports/surgical-suction-instruments-market-129636225.html The global surgical suction instruments market is projected to reach 503 million in 2029 from USD 375 million in 2024, at a CAGR of 6.1% between 2024 and 2029. The rising technological advancemnets and increasing geriatric population is driving the growth of the market. As the global population ages, the number of chronic diseases is increasing which is expected to drive the market growth. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=129636225 Elderly patients often experience age-related decline in appetite or swallowing difficulties, making enteral feeding a vital support system. Based on type, the surgical suction instruments market is segmented into retractors, yankauer suction tube, poole suction tube, frazier suction tip, others. The yankauer suction tube accounts for the largest share in the surgical suction instruments market, the bulbous tip design and wide opening allow for efficient suction of blood, fluids, and debris from the surgical field. This improves visibility and reduces the risk of obscuring critical structures. which is expected to drive the segment growth. Based on application, the surgical suction instruments market is segmented into general surgery, neurosurgery, orthopedic surgery, cardiovascular surgery, dental surgery. The general surgery accounts for the largest share in the surgical suction instruments market, Surgical suction instruments play a vital role in various aspects of general surgery, contributing to a clean and efficient operative environment. Suction removes blood, fluids, and debris from the surgical site, allowing the surgeon a clear view of the underlying anatomy. This is crucial for precise dissection, minimizing the risk of unintended injury to vital structures which is expected to drive the market growth. In 2023, North America accounted for the largest share of the surgical suction instruments market, followed by Europe and Asia Pacific. The United States and Canada have well-equipped hospitals and a strong focus on advanced medical care, which supports the adoption of surgical suction instruments, also compared to established markets like North America and Europe, the Asia Pacific region often offers lower labor costs, making it an attractive option for companies seeking to optimize manufacturing expenses. The major players in the surgical suction instruments market include include The prominent players in the medical device contract manufacturing market include include Olympus (Japan), Cardinal Health, Inc. (US), Stryker Corporation (US), Medtronic (Ireland), B. Braun Melsungen AG (Germany), CONMED Corporation (US), BD (US), Steris Plc (Ireland), Teleflex Incorporated (US), Carl Zeiss Meditech AG (Germany), Integra Lifesciences Holdings Corporation (US), KARL STORZ SE & CO. KG (Germany), Indosurgicals Private Limited (India), Applied Medical Technology, Inc. (US), Amsino International, Inc.(US), Surtex Instruments Limited (UK), Bionix LLC.(US), Vactechindia.Com (India), Applied Medical Resources Corporation (US), DTR Medical Ltd (UK), Sklar Surgical Instruments (US), PAJUNK (Germany), Hangzhou Kangji Medical Instrument Co.,Ltd.(China), Romsons (India), Narang Medical Limited.(India). Recent Developments of the Surgical Suction Instruments Industry: In January 2024, Olympus Corporation acquired the Taewoong Medical Co., Ltd., a Korea-based manufacturer of medical devices. This acquisition helps Olympus to strengthen its GI Endo Therapy product portfolio capabilities, contribute to improving patient outcomes through comprehensive solutions, and elevate the standard of care. In May 2023, Stryker acquired the Cerus Endovascular Ltd. (UK), a medical device company engaged in the design and development of neurointerventional devices. Cerus Endovascular’s marked products, helped to expand Stryker’s current portfolio of aneurysm treatment solutions. In September 2022, Cardinal Health, Inc. (US) announced the partnership with Kinaxis (Canada) to enhance the Kinaxis RapidResponse Platform used for supply chain agility and medical product visibility. In July 2022, Medtronic and the American Society for Gastrointestinal Endoscopy expanded the Health Equity Assistance Program for colon cancer screening with support from Amazon Web Services. Completed first installation of donated GI Genius intelligent endoscopy modules. -

-

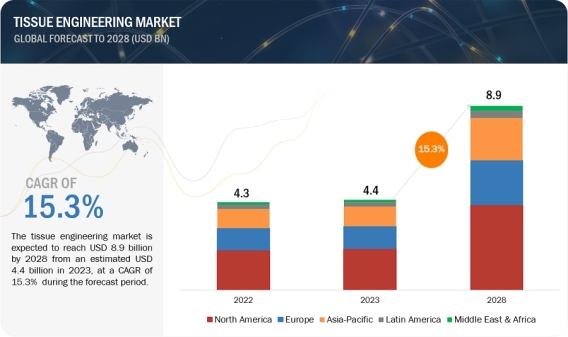

Driving Regenerative Medicine Advances: Tissue Engineering Market to Reach $8.9 Billion by 2028 https://www.marketsandmarkets.com/Market-Reports/tissue-engineering-market-34135173.html The tissue engineering market is expected to reach USD 8.9 billion by 2028 from an estimated USD 4.4 billion in 2023, at a CAGR of 15.3% during the forecast period. The growth is attributed to numerous factors including increasing incidences of road accidents, rising demand for regenerative medicines for the treatment of chronic diseases, and growing technological advancements in the biopharmaceutical sector. In addition, increasing research activities in the field of tissue engineering is promoting the growth of the tissue engineering market. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=34135173 3D bioprinting is an innovative technology in tissue engineering, that enables the precise fabrication of intricate tissue structures, vital for regenerative medicine and drug testing. Its development is primarily propelled by continual technological advancements, including improved bio inks and printing techniques, coupled with the critical need to address organ shortages and revolutionize medical treatments. Material innovation also plays a pivotal role, in fostering the creation of biocompatible substances essential for enhancing the viability and functionality of bio-printed tissues. Additionally, collaborative research efforts among multidisciplinary fields drive progress, promising transformative solutions in healthcare. Based on product type, the tissue engineering market has been segmented into scaffolds, tissue grafts, and other products. In 2022, scaffolds accounted for the largest market share. Scaffold-driven tissue engineering hinges on biocompatibility, mechanical robustness, and optimal pore structure for cell infiltration and nutrient exchange. Integration of bioactive cues and vascular-like properties also fuels advancements, crucial for crafting functional and viable engineered tissues. These driving factors collectively shape scaffold design, influencing their efficacy in tissue engineering applications. Based on material, the global tissue engineering market is segmented into synthetic materials and biologically derived materials. Synthetic material accounted for major market share of the tissue engineering market in 2022. The large share of this segment can be attributed to the cost effectiveness of the synthetic products as compared to the biologically derived products. In addition, increasing demand for advanced and cost-effective tissue engineering solutions is propelling the growth of the synthetic material segment in the tissue engineering market. Based on application, the tissue engineering market is segmented into orthopedics & musculoskeletal disorders, dermatology & wound care, dental disorders, cardiovascular diseases, and others. In 2022, orthopedics & musculoskeletal disorders accounted for the largest share of the global tissue engineering market. The large share of the segment can primarily be attributed to rising demand for high quality tissue engineering products for the repair and reconstruction of damaged tissues or organs. Additionally, increasing incidences of road accidents are promoting the adoption of tissue engineering products for tissue reconstruction. Based on end users, the tissue engineering market has been segmented into hospitals, specialty centers and clinics, and ambulatory surgical centers. Hospitals accounted for the largest market share of the tissue engineering market. The large share of the segment can primarily be attributed to the increasing demand for advanced regeneration solutions for the reconstruction and regeneration of tissues. Additionally, the increasing rate of chronic and degenerative diseases is driving the demand for hospitals. The key regional markets for the global tissue engineering market are Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa. In 2022, North America accounted for the largest share of the market. The large share of this region can be attributed to the growing technological developments in the healthcare sector and rising research activities for the advancements of the tissue engineering field. However, most of the growth in the market is expected from emerging countries across Asia Pacific. During the forecast period, the Asia Pacific is expected to grow with the fastest CAGR due to the increasing adoption of innovative technologies for the treatment of chronic and degenerative diseases. Key players in the global tissue engineering market include Organogenesis (US), AbbVie Inc. (US), Baxter (US), BD (US), B. Braun (Germany), TEIJIN Limited (Japan), Institut Straumann AG (Switzerland), Integra Lifesciences (US), Johnson & Johnson Services, Inc. (US), Medtronic (Ireland), NuVasive, Inc. (US), Stryker (US), Terumo Corporation (Japan), W. L. Gore & Associates Inc. (US), Zimmer Biomet (US), Smith & Nephew plc (UK), MIMEDX Group, Inc. (US), BioTissue (US), CollPlant Biotechnologies Ltd. (Israel), Sumitomo Pharma Co., Ltd. (Japan), Matricel GmbH (Germany), Mallinckrodt (US), Regrow Biosciences Pvt Ltd (India), Vericel Corporation (US), Tecnoss S.R.L. (Italy), Tegoscience (South Korea), and Tissue Regenix (UK). Recent Developments of Tissue Engineering Industry In September 2023, MIMEDX Group Inc. launched EPIEFFECT to broaden its advanced wound care product portfolio. EPIEFFECT is a lyophilized human placental-based allograft consisting of amnion and chorion membranes. In July 2023, Teijin Limited launched SYNFOLIUM, a cardiovascular surgical patch and received manufacturing and marketing approval in Japan. The cardiovascular surgical patch is used for the surgical treatment of congenital heart disease (CHD). In July 2021, Integra Lifesciences introduced SurgiMend, a collagen matrix. The product is used for soft tissue repair and reconstruction. In May 2020, AbbVie Inc. (US) acquired Allergan plc (Ireland) to expand the product portfolio in therapeutics categories. Allergan plc provides new growth opportunities to AbbVie Inc. in neuroscience with Vraylar, Botox therapeutics, and global aesthetics business.

Driving Regenerative Medicine Advances: Tissue Engineering Market to Reach $8.9 Billion by 2028 https://www.marketsandmarkets.com/Market-Reports/tissue-engineering-market-34135173.html The tissue engineering market is expected to reach USD 8.9 billion by 2028 from an estimated USD 4.4 billion in 2023, at a CAGR of 15.3% during the forecast period. The growth is attributed to numerous factors including increasing incidences of road accidents, rising demand for regenerative medicines for the treatment of chronic diseases, and growing technological advancements in the biopharmaceutical sector. In addition, increasing research activities in the field of tissue engineering is promoting the growth of the tissue engineering market. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=34135173 3D bioprinting is an innovative technology in tissue engineering, that enables the precise fabrication of intricate tissue structures, vital for regenerative medicine and drug testing. Its development is primarily propelled by continual technological advancements, including improved bio inks and printing techniques, coupled with the critical need to address organ shortages and revolutionize medical treatments. Material innovation also plays a pivotal role, in fostering the creation of biocompatible substances essential for enhancing the viability and functionality of bio-printed tissues. Additionally, collaborative research efforts among multidisciplinary fields drive progress, promising transformative solutions in healthcare. Based on product type, the tissue engineering market has been segmented into scaffolds, tissue grafts, and other products. In 2022, scaffolds accounted for the largest market share. Scaffold-driven tissue engineering hinges on biocompatibility, mechanical robustness, and optimal pore structure for cell infiltration and nutrient exchange. Integration of bioactive cues and vascular-like properties also fuels advancements, crucial for crafting functional and viable engineered tissues. These driving factors collectively shape scaffold design, influencing their efficacy in tissue engineering applications. Based on material, the global tissue engineering market is segmented into synthetic materials and biologically derived materials. Synthetic material accounted for major market share of the tissue engineering market in 2022. The large share of this segment can be attributed to the cost effectiveness of the synthetic products as compared to the biologically derived products. In addition, increasing demand for advanced and cost-effective tissue engineering solutions is propelling the growth of the synthetic material segment in the tissue engineering market. Based on application, the tissue engineering market is segmented into orthopedics & musculoskeletal disorders, dermatology & wound care, dental disorders, cardiovascular diseases, and others. In 2022, orthopedics & musculoskeletal disorders accounted for the largest share of the global tissue engineering market. The large share of the segment can primarily be attributed to rising demand for high quality tissue engineering products for the repair and reconstruction of damaged tissues or organs. Additionally, increasing incidences of road accidents are promoting the adoption of tissue engineering products for tissue reconstruction. Based on end users, the tissue engineering market has been segmented into hospitals, specialty centers and clinics, and ambulatory surgical centers. Hospitals accounted for the largest market share of the tissue engineering market. The large share of the segment can primarily be attributed to the increasing demand for advanced regeneration solutions for the reconstruction and regeneration of tissues. Additionally, the increasing rate of chronic and degenerative diseases is driving the demand for hospitals. The key regional markets for the global tissue engineering market are Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa. In 2022, North America accounted for the largest share of the market. The large share of this region can be attributed to the growing technological developments in the healthcare sector and rising research activities for the advancements of the tissue engineering field. However, most of the growth in the market is expected from emerging countries across Asia Pacific. During the forecast period, the Asia Pacific is expected to grow with the fastest CAGR due to the increasing adoption of innovative technologies for the treatment of chronic and degenerative diseases. Key players in the global tissue engineering market include Organogenesis (US), AbbVie Inc. (US), Baxter (US), BD (US), B. Braun (Germany), TEIJIN Limited (Japan), Institut Straumann AG (Switzerland), Integra Lifesciences (US), Johnson & Johnson Services, Inc. (US), Medtronic (Ireland), NuVasive, Inc. (US), Stryker (US), Terumo Corporation (Japan), W. L. Gore & Associates Inc. (US), Zimmer Biomet (US), Smith & Nephew plc (UK), MIMEDX Group, Inc. (US), BioTissue (US), CollPlant Biotechnologies Ltd. (Israel), Sumitomo Pharma Co., Ltd. (Japan), Matricel GmbH (Germany), Mallinckrodt (US), Regrow Biosciences Pvt Ltd (India), Vericel Corporation (US), Tecnoss S.R.L. (Italy), Tegoscience (South Korea), and Tissue Regenix (UK). Recent Developments of Tissue Engineering Industry In September 2023, MIMEDX Group Inc. launched EPIEFFECT to broaden its advanced wound care product portfolio. EPIEFFECT is a lyophilized human placental-based allograft consisting of amnion and chorion membranes. In July 2023, Teijin Limited launched SYNFOLIUM, a cardiovascular surgical patch and received manufacturing and marketing approval in Japan. The cardiovascular surgical patch is used for the surgical treatment of congenital heart disease (CHD). In July 2021, Integra Lifesciences introduced SurgiMend, a collagen matrix. The product is used for soft tissue repair and reconstruction. In May 2020, AbbVie Inc. (US) acquired Allergan plc (Ireland) to expand the product portfolio in therapeutics categories. Allergan plc provides new growth opportunities to AbbVie Inc. in neuroscience with Vraylar, Botox therapeutics, and global aesthetics business. -

-

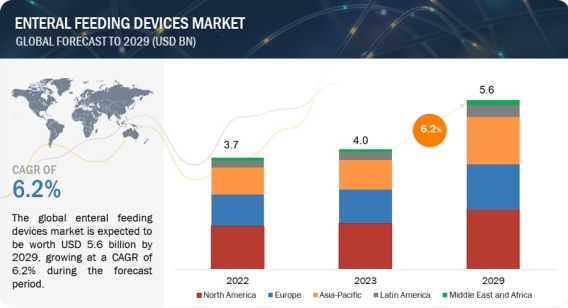

Global Enteral Feeding Devices Market Worth $5.6 Billion by 2029: Key Insights and Analysis https://www.marketsandmarkets.com/Market-Reports/enteral-feeding-device-market-183623035.html The global enteral feeding devices market is projected to reach 5.6 billion in 2029 from USD 4.0 billion in 2023, at a CAGR of 6.2% between 2023 and 2029. The rising technological advancemnets and increasing geriatric population is driving the growth of the market. The As the global population ages, the number of individuals requiring enteral feeding is expected to rise. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=183623035 Elderly patients often experience age-related decline in appetite or swallowing difficulties, making enteral feeding a vital support system. Based on type, the enteral feeding devices market is segmented into enteral feeding tubes, enteral feeding pumps, administration sets, enteral syringes and consumables. The enteral feeding tubes accounts for the largest share in the enteral feeding devices market, Enteral feeding tubes are a crucial component of enteral feeding devices. They act as a conduit to deliver liquid nutrition directly into a patient's stomach or small intestine, bypassing the mouth and esophagus. Enteral feeding tubes are essential components of enteral feeding devices, providing a safe and reliable way to deliver essential nutrients to patients who cannot consume food orally which is expected to drive the segment growth. Based on application, the enteral feeding devices market is segmented into oncology, gastrointestinal diseases, nuerological diseases, diabetes, hypermetabolism and other applications. The oncology accounts for the largest share in the enteral feeding devices market, cancer and its treatment (surgery, radiation, chemotherapy) can significantly impact a patient's appetite and ability to absorb nutrients. Enteral feeding ensures they receive the necessary calories, proteins, vitamins, and minerals to support their immune system, fight infection, and promote healing which is expected to drive the market growth. In 2023, North America accounted for the largest share of the enteral feeding devices market, followed by Europe and Asia Pacific. The United States and Canada have well-equipped hospitals and a strong focus on advanced medical care, which supports the adoption of enteral feeding devices, also compared to established markets like North America and Europe, the Asia Pacific region often offers lower labor costs, making it an attractive option for companies seeking to optimize manufacturing expenses. Additionally, several countries in the region, like China and India, have developed a robust infrastructure for manufacturing pharmaceuticals and medical devices which is expected to lead to Asia Pacific growing at the fastest rate during the forecast period. The major players in the enteral feeding devices market include include The prominent players in the medical device contract manufacturing market include Fresenius SE & Co. KGAA (Germany), Cardinal Health, Inc. (US), Nestlé S.A. (Switzerland), Avanos Medical, Inc. (US), Danone S.A. (France), Becton, Dickinson and Company (US), B. Braun Melsungen AG (Germany), CONMED Corporation (US), Cook Medical (US), Moog Inc. (US), Boston Scientific Corporation (US), Baxter International Inc. (US), Vygon (France), and Other players in the enteral feeding devices market are Applied Medical Technology (US), Amsino International Inc. (US), Omex Medical Technology (India), Danumed Medizintechnik (Germany), Medline Industries, Inc. (US), Fuji Systems (Japan), Kentec Medical (US), Dynarex Corporation (US), Vesco Medical LLC (US), Medela AG (Switzerland), Alcor Scientific (US), and Romsons (India) Recent Developments of Enteral Feeding Devices Industry: In September 2022, Cardinal Health, Inc. (US) announced the partnership with Kinaxis (Canada) to enhance the Kinaxis RapidResponse Platform used for supply chain agility and medical product visibility. In November 2022, Boston Scientific signed an agreement for the acquisition of Apollo Endosurgery, Inc.,. This agreement includes devices, which are used during endoluminal surgery (ELS) procedures, to close gastrointestinal defects, manage gastrointestinal complications, and aid in weight loss for patients suffering from obesity. In March 2021, Applied Medical Technology, Inc. (US) launched its gastric-jejunal enteral feeding tube family (G-JETs) to include the low-profile micro-G-JET to link up the enteral nutrition needs of pediatric patients. In March 2022, Vygon Group (France) announced the acquisition of distributor Macatt Medica (Peru). The acquisition is expected to grow the presence of Vygon Group (France), in the South American region, specifically for its broad range of enteral feeding products.

Global Enteral Feeding Devices Market Worth $5.6 Billion by 2029: Key Insights and Analysis https://www.marketsandmarkets.com/Market-Reports/enteral-feeding-device-market-183623035.html The global enteral feeding devices market is projected to reach 5.6 billion in 2029 from USD 4.0 billion in 2023, at a CAGR of 6.2% between 2023 and 2029. The rising technological advancemnets and increasing geriatric population is driving the growth of the market. The As the global population ages, the number of individuals requiring enteral feeding is expected to rise. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=183623035 Elderly patients often experience age-related decline in appetite or swallowing difficulties, making enteral feeding a vital support system. Based on type, the enteral feeding devices market is segmented into enteral feeding tubes, enteral feeding pumps, administration sets, enteral syringes and consumables. The enteral feeding tubes accounts for the largest share in the enteral feeding devices market, Enteral feeding tubes are a crucial component of enteral feeding devices. They act as a conduit to deliver liquid nutrition directly into a patient's stomach or small intestine, bypassing the mouth and esophagus. Enteral feeding tubes are essential components of enteral feeding devices, providing a safe and reliable way to deliver essential nutrients to patients who cannot consume food orally which is expected to drive the segment growth. Based on application, the enteral feeding devices market is segmented into oncology, gastrointestinal diseases, nuerological diseases, diabetes, hypermetabolism and other applications. The oncology accounts for the largest share in the enteral feeding devices market, cancer and its treatment (surgery, radiation, chemotherapy) can significantly impact a patient's appetite and ability to absorb nutrients. Enteral feeding ensures they receive the necessary calories, proteins, vitamins, and minerals to support their immune system, fight infection, and promote healing which is expected to drive the market growth. In 2023, North America accounted for the largest share of the enteral feeding devices market, followed by Europe and Asia Pacific. The United States and Canada have well-equipped hospitals and a strong focus on advanced medical care, which supports the adoption of enteral feeding devices, also compared to established markets like North America and Europe, the Asia Pacific region often offers lower labor costs, making it an attractive option for companies seeking to optimize manufacturing expenses. Additionally, several countries in the region, like China and India, have developed a robust infrastructure for manufacturing pharmaceuticals and medical devices which is expected to lead to Asia Pacific growing at the fastest rate during the forecast period. The major players in the enteral feeding devices market include include The prominent players in the medical device contract manufacturing market include Fresenius SE & Co. KGAA (Germany), Cardinal Health, Inc. (US), Nestlé S.A. (Switzerland), Avanos Medical, Inc. (US), Danone S.A. (France), Becton, Dickinson and Company (US), B. Braun Melsungen AG (Germany), CONMED Corporation (US), Cook Medical (US), Moog Inc. (US), Boston Scientific Corporation (US), Baxter International Inc. (US), Vygon (France), and Other players in the enteral feeding devices market are Applied Medical Technology (US), Amsino International Inc. (US), Omex Medical Technology (India), Danumed Medizintechnik (Germany), Medline Industries, Inc. (US), Fuji Systems (Japan), Kentec Medical (US), Dynarex Corporation (US), Vesco Medical LLC (US), Medela AG (Switzerland), Alcor Scientific (US), and Romsons (India) Recent Developments of Enteral Feeding Devices Industry: In September 2022, Cardinal Health, Inc. (US) announced the partnership with Kinaxis (Canada) to enhance the Kinaxis RapidResponse Platform used for supply chain agility and medical product visibility. In November 2022, Boston Scientific signed an agreement for the acquisition of Apollo Endosurgery, Inc.,. This agreement includes devices, which are used during endoluminal surgery (ELS) procedures, to close gastrointestinal defects, manage gastrointestinal complications, and aid in weight loss for patients suffering from obesity. In March 2021, Applied Medical Technology, Inc. (US) launched its gastric-jejunal enteral feeding tube family (G-JETs) to include the low-profile micro-G-JET to link up the enteral nutrition needs of pediatric patients. In March 2022, Vygon Group (France) announced the acquisition of distributor Macatt Medica (Peru). The acquisition is expected to grow the presence of Vygon Group (France), in the South American region, specifically for its broad range of enteral feeding products. -

-

Innovations in Digital Diabetes Management: Transforming Patient Care https://www.marketsandmarkets.com/Market-Reports/digital-diabetes-management-market-144725893.html The global digital diabetes management market is projected to reach USD 35.8 Billion by 2028 from an estimated USD 18.9 Billion in 2023, at a CAGR of 13.6% during the forecast period. The growing number of people with diabetes has led to an increased focus on developing and adopting better diabetes care solutions. Advances in technology have made it possible to create more flexible and sophisticated solutions. The increasing use of cloud-based enterprise solutions and connected devices and apps are also driving market growth. However, high device costs, lack of reimbursement in developing countries, and the preference for traditional diabetes management devices are expected to slow market growth. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=144725893 The digital diabetes management market offers a wide range of devices, apps, data management software & platforms, and services. Smart glucose metres, continuous glucose monitoring (CGM) systems, smart insulin pens, smart insulin pumps/closed-loop systems, and smart insulin patches are included in the devices segment. Similarly, the digital diabetes management apps segment is further sub-segmented into diabetes & blood glucose tracking apps and obesity & diet management apps. In 2022, the devices segment held the largest market share for digital diabetes management, with 76.4%. Factors such as the increasing demand for wireless and wearable devices for diabetes management, growing acceptance of smart insulin pumps & pens for insulin delivery, and the growing awareness about continuous glucose monitoring in patients are driving the market growth. Different types of digital diabetes management device studied in the report are handheld devices and wearable devices. Among these, the The market for digital diabetes management devices in 2022 was dominated by wearables, with a share of 60.3%. By 2028, this market is expected to have grown from USD 8,876.3 million in 2023 to USD 18,557.3 million. Technology advancements like closed-loop pump systems, smart insulin patches, and other pipeline devices, as well as factors like the growing use of smart insulin pumps and insulin patches for self-insulin delivery in diabetes management, are all the factors that are boosting the wearable devices segment's growth.. Various end users of the digital diabetes management market are self/home healthcare, hospitals & specialty diabetes clinics, and academic & research institutes. The self/home healthcare accounted for the largest share of 79.9% of the digital diabetes management market in 2022. The large share of this segment can mainly be credited to technological advancements and a shift toward home care and self-management of diabetes. North America is estimated to grow at the highest CAGR during the forecast period. The region also accounted for the largest market share of 45.3%, followed by Europe with a share of 28.1% in 2022. Various factors attributing to the growth of the digital diabetes management market in North America are growing adoption of connected diabetes management devices, high adoption of diabetes management apps, growing demand for integrated hybrid closed-loop systems, favorable reimbursement policies, and government initiatives to promote digital health in the region. Furthermore, In Asia Pacific, countries such as China and India have a high prevalence rate of diabetes, primarily due to the increasing urbanization, population and lifestyle changes. The increasing incidence of diabetes, rising awareness, high undiagnosed population, and the rising penetration of smartphones and tablets have propelled the adoption of digital diabetes management solutions in the region. The prominent players operating in the global digital diabetes management market are Medtronic (Ireland), B. Braun Melsungen AG (Germany), Dexcom, Inc. (US), Abbott Laboratories (US), F. Hoffmann-La Roche (Switzerland), Insulet Corporation (US), Tandem Diabetes Care (US), Ascensia Diabetes Care Holdings AG (Switzerland), LifeScan, Inc. (US), Tidepool (US), AgaMatrix (US), Glooko, Inc. (US), DarioHealth Corporation (Israel), One Drop (US), Dottli (Finland), Ypsomed Holding AG (Switzerland), ARKRAY (Japan), ACON Laboratories, Inc. (US), Care Innovations, LLC (US), Health2Sync (Taiwan), Emperra GmbH E-Health Technologies (Germany), Azumio (US), Decide Clinical Software GmbH (Austria), Pendiq GmbH (Germany), and BeatO (India). Recent Developments of Digital Diabetes Management Industry In February 2023, Dexcom launched Dexcom G7 CGM device in the US and is planning to launch in Europe and Asia Pacific by first quarter of 2024 In October 2022, Abbott laboratories launched Freestyle Libre 3 CGM device worldwide. In April 2022, Dexcom launched Dexcom ONE device. The company launched the new Dexcom ONE Continuous Glucose Monitoring System in the UK. In April 2022, Ascensia Diabetes Care Holdings AG (Switzerland) launched Eversense's 6-month CGM system in the US. In October 2021, LifeScan, Inc. (US) launched OneTouch Solutions. This is a holistic digital health offering linking people with diabetes to solutions and support from proven experts. In September 2020, Roche Diagnostics (Switzerland) launched a remote patient monitoring ssolution, which is a new element of the RocheDiabetes Care Platform and uses its pattern detection feature.

Innovations in Digital Diabetes Management: Transforming Patient Care https://www.marketsandmarkets.com/Market-Reports/digital-diabetes-management-market-144725893.html The global digital diabetes management market is projected to reach USD 35.8 Billion by 2028 from an estimated USD 18.9 Billion in 2023, at a CAGR of 13.6% during the forecast period. The growing number of people with diabetes has led to an increased focus on developing and adopting better diabetes care solutions. Advances in technology have made it possible to create more flexible and sophisticated solutions. The increasing use of cloud-based enterprise solutions and connected devices and apps are also driving market growth. However, high device costs, lack of reimbursement in developing countries, and the preference for traditional diabetes management devices are expected to slow market growth. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=144725893 The digital diabetes management market offers a wide range of devices, apps, data management software & platforms, and services. Smart glucose metres, continuous glucose monitoring (CGM) systems, smart insulin pens, smart insulin pumps/closed-loop systems, and smart insulin patches are included in the devices segment. Similarly, the digital diabetes management apps segment is further sub-segmented into diabetes & blood glucose tracking apps and obesity & diet management apps. In 2022, the devices segment held the largest market share for digital diabetes management, with 76.4%. Factors such as the increasing demand for wireless and wearable devices for diabetes management, growing acceptance of smart insulin pumps & pens for insulin delivery, and the growing awareness about continuous glucose monitoring in patients are driving the market growth. Different types of digital diabetes management device studied in the report are handheld devices and wearable devices. Among these, the The market for digital diabetes management devices in 2022 was dominated by wearables, with a share of 60.3%. By 2028, this market is expected to have grown from USD 8,876.3 million in 2023 to USD 18,557.3 million. Technology advancements like closed-loop pump systems, smart insulin patches, and other pipeline devices, as well as factors like the growing use of smart insulin pumps and insulin patches for self-insulin delivery in diabetes management, are all the factors that are boosting the wearable devices segment's growth.. Various end users of the digital diabetes management market are self/home healthcare, hospitals & specialty diabetes clinics, and academic & research institutes. The self/home healthcare accounted for the largest share of 79.9% of the digital diabetes management market in 2022. The large share of this segment can mainly be credited to technological advancements and a shift toward home care and self-management of diabetes. North America is estimated to grow at the highest CAGR during the forecast period. The region also accounted for the largest market share of 45.3%, followed by Europe with a share of 28.1% in 2022. Various factors attributing to the growth of the digital diabetes management market in North America are growing adoption of connected diabetes management devices, high adoption of diabetes management apps, growing demand for integrated hybrid closed-loop systems, favorable reimbursement policies, and government initiatives to promote digital health in the region. Furthermore, In Asia Pacific, countries such as China and India have a high prevalence rate of diabetes, primarily due to the increasing urbanization, population and lifestyle changes. The increasing incidence of diabetes, rising awareness, high undiagnosed population, and the rising penetration of smartphones and tablets have propelled the adoption of digital diabetes management solutions in the region. The prominent players operating in the global digital diabetes management market are Medtronic (Ireland), B. Braun Melsungen AG (Germany), Dexcom, Inc. (US), Abbott Laboratories (US), F. Hoffmann-La Roche (Switzerland), Insulet Corporation (US), Tandem Diabetes Care (US), Ascensia Diabetes Care Holdings AG (Switzerland), LifeScan, Inc. (US), Tidepool (US), AgaMatrix (US), Glooko, Inc. (US), DarioHealth Corporation (Israel), One Drop (US), Dottli (Finland), Ypsomed Holding AG (Switzerland), ARKRAY (Japan), ACON Laboratories, Inc. (US), Care Innovations, LLC (US), Health2Sync (Taiwan), Emperra GmbH E-Health Technologies (Germany), Azumio (US), Decide Clinical Software GmbH (Austria), Pendiq GmbH (Germany), and BeatO (India). Recent Developments of Digital Diabetes Management Industry In February 2023, Dexcom launched Dexcom G7 CGM device in the US and is planning to launch in Europe and Asia Pacific by first quarter of 2024 In October 2022, Abbott laboratories launched Freestyle Libre 3 CGM device worldwide. In April 2022, Dexcom launched Dexcom ONE device. The company launched the new Dexcom ONE Continuous Glucose Monitoring System in the UK. In April 2022, Ascensia Diabetes Care Holdings AG (Switzerland) launched Eversense's 6-month CGM system in the US. In October 2021, LifeScan, Inc. (US) launched OneTouch Solutions. This is a holistic digital health offering linking people with diabetes to solutions and support from proven experts. In September 2020, Roche Diagnostics (Switzerland) launched a remote patient monitoring ssolution, which is a new element of the RocheDiabetes Care Platform and uses its pattern detection feature. -

-

Rising Demand in Orthopedics to Drive Cartilage Repair/Regeneration Market to $2.8 Billion by 2028 https://www.marketsandmarkets.com/Market-Reports/cartilage-repair-regeneration-market-37493272.html The global Cartilage Repair/Cartilage Regeneration market is projected to reach USD 2.8 Billion by 2028 from USD 1.3 Billion in 2023, at a CAGR of 17.2% during the forecast period. Growth in the Cartilage Repair/Cartilage Regeneration market is mainly driven by the Increasing incidence of osteoarthritis, Increasing research funding and investments and the Rising number of sports and accident-related orthopedic injuries expected to grow the market demand Cartilage Repair/Cartilage Regeneration market during the forecast period. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=37493272 Based on the treatment modality, the cartilage repair/cartilage regeneration market is divided into two categories which are cell-based including chondrocyte transplantation, growth factors, and stem cells and non-cell-based like tissue scaffolds and cell-free composites. In 2022, the cell-based segment had the largest share in the treatment modality segment which is mainly due to advancements in stem cell- therapies used for cartilage repair. Based on the Application site, the cartilage repair/cartilage regeneration market is categorized into knees, hips, ankles & feet, and other application sites like nose and shoulder. In 2022, The knee segment holds the largest share of the cartilage repair/cartilage regeneration market. The factors responsible for the growth of the segment are the increasing number of knee arthroscopy procedures and the rising incidence of knee osteoarthritis cases globally. Based on the Application, the global cartilage repair/cartilage regeneration market is broadly segmented into hyaline cartilage and fibrocartilage. The hyaline cartilage segment accounted for the largest share of the cartilage repair and regeneration market in 2022. Hyaline cartilage is expected to grow highest in the upcoming years due to the increasing number of cartilage repair procedures performed worldwide is the major factor driving the growth of this application segment. Technological advancements, product developments and launches, and growing partnerships between key market players and hospitals are also supporting market growth. Based on the region segmentation, the cartilage repair/cartilage regeneration market is divided into North America, Europe, Asia Pacific, and the Rest of the World. North America holds the largest share and expects to dominate the cartilage repair/cartilage regeneration market. Growth in the North American market is mainly driven by the rising growth opportunities in emerging economies and growing number of contracts and agreements between market players. Major Companies: Smith+Nephew (UK), DePuy Synthes (Johnson & Johnson) (US), Zimmer Biomet Holdings, Inc. (US), Stryker Corporation (US), Vericel Corporation (US), B. Braun Melsungen AG (US), Anika Therapeutics (US), CONMED Corporation (US), MEDIPOST (South Korea), RTI Surgical (US), Arthrex, Inc. (US), Regrow Biosciences (India), Geistlich Pharma AG (Switzerland), AlloSource (US), Orthocell Ltd, (Australia), Matricel GmbH (Germany), CartiHeal, Inc. (Israel), Regentis Biomaterials (Israel), Theracell Advanced Biotechnology (Greece), and LifeNet Health (US) The objective of the study is to analyze the key market dynamics, such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as acquisitions, product launches, expansions, collaborations, agreements, and partnerships of the leading players, the competitive landscape of the cartilage repair/cartilage regeneration market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches were used to estimate the market size. To estimate the market size of segments and subsegments, the market breakdown and data triangulation were used. The four steps involved in estimating the market size are: Collecting Secondary Data The secondary research data collection process involves the usage of secondary sources, directories, databases (such as Bloomberg Businessweek, Factiva, and D&B), annual reports, investor presentations, and SEC filings of companies. Secondary research was used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the cartilage repair/cartilage regeneration market. A database of the key industry leaders was also prepared using secondary research. Collecting Primary Data The primary research data was collected after acquiring knowledge about the cartilage repair/cartilage regeneration market scenario through secondary research. A significant number of primary interviews were conducted with stakeholders from both the demand side (such as Hospitals) and supply side (such as included various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing, and product development teams, product manufacturers, wholesalers, channel partners, and distributors) across major countries of North America, Europe, Asia Pacific and Rest of the world. Approximately 40% of the primary interviews were conducted with stakeholders from the demand side, while those from the supply side accounted for the remaining 60%. Primary data for this report was collected through questionnaires, emails, and telephonic interviews.

Rising Demand in Orthopedics to Drive Cartilage Repair/Regeneration Market to $2.8 Billion by 2028 https://www.marketsandmarkets.com/Market-Reports/cartilage-repair-regeneration-market-37493272.html The global Cartilage Repair/Cartilage Regeneration market is projected to reach USD 2.8 Billion by 2028 from USD 1.3 Billion in 2023, at a CAGR of 17.2% during the forecast period. Growth in the Cartilage Repair/Cartilage Regeneration market is mainly driven by the Increasing incidence of osteoarthritis, Increasing research funding and investments and the Rising number of sports and accident-related orthopedic injuries expected to grow the market demand Cartilage Repair/Cartilage Regeneration market during the forecast period. Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=37493272 Based on the treatment modality, the cartilage repair/cartilage regeneration market is divided into two categories which are cell-based including chondrocyte transplantation, growth factors, and stem cells and non-cell-based like tissue scaffolds and cell-free composites. In 2022, the cell-based segment had the largest share in the treatment modality segment which is mainly due to advancements in stem cell- therapies used for cartilage repair. Based on the Application site, the cartilage repair/cartilage regeneration market is categorized into knees, hips, ankles & feet, and other application sites like nose and shoulder. In 2022, The knee segment holds the largest share of the cartilage repair/cartilage regeneration market. The factors responsible for the growth of the segment are the increasing number of knee arthroscopy procedures and the rising incidence of knee osteoarthritis cases globally. Based on the Application, the global cartilage repair/cartilage regeneration market is broadly segmented into hyaline cartilage and fibrocartilage. The hyaline cartilage segment accounted for the largest share of the cartilage repair and regeneration market in 2022. Hyaline cartilage is expected to grow highest in the upcoming years due to the increasing number of cartilage repair procedures performed worldwide is the major factor driving the growth of this application segment. Technological advancements, product developments and launches, and growing partnerships between key market players and hospitals are also supporting market growth. Based on the region segmentation, the cartilage repair/cartilage regeneration market is divided into North America, Europe, Asia Pacific, and the Rest of the World. North America holds the largest share and expects to dominate the cartilage repair/cartilage regeneration market. Growth in the North American market is mainly driven by the rising growth opportunities in emerging economies and growing number of contracts and agreements between market players. Major Companies: Smith+Nephew (UK), DePuy Synthes (Johnson & Johnson) (US), Zimmer Biomet Holdings, Inc. (US), Stryker Corporation (US), Vericel Corporation (US), B. Braun Melsungen AG (US), Anika Therapeutics (US), CONMED Corporation (US), MEDIPOST (South Korea), RTI Surgical (US), Arthrex, Inc. (US), Regrow Biosciences (India), Geistlich Pharma AG (Switzerland), AlloSource (US), Orthocell Ltd, (Australia), Matricel GmbH (Germany), CartiHeal, Inc. (Israel), Regentis Biomaterials (Israel), Theracell Advanced Biotechnology (Greece), and LifeNet Health (US) The objective of the study is to analyze the key market dynamics, such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as acquisitions, product launches, expansions, collaborations, agreements, and partnerships of the leading players, the competitive landscape of the cartilage repair/cartilage regeneration market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches were used to estimate the market size. To estimate the market size of segments and subsegments, the market breakdown and data triangulation were used. The four steps involved in estimating the market size are: Collecting Secondary Data The secondary research data collection process involves the usage of secondary sources, directories, databases (such as Bloomberg Businessweek, Factiva, and D&B), annual reports, investor presentations, and SEC filings of companies. Secondary research was used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the cartilage repair/cartilage regeneration market. A database of the key industry leaders was also prepared using secondary research. Collecting Primary Data The primary research data was collected after acquiring knowledge about the cartilage repair/cartilage regeneration market scenario through secondary research. A significant number of primary interviews were conducted with stakeholders from both the demand side (such as Hospitals) and supply side (such as included various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing, and product development teams, product manufacturers, wholesalers, channel partners, and distributors) across major countries of North America, Europe, Asia Pacific and Rest of the world. Approximately 40% of the primary interviews were conducted with stakeholders from the demand side, while those from the supply side accounted for the remaining 60%. Primary data for this report was collected through questionnaires, emails, and telephonic interviews. -

-

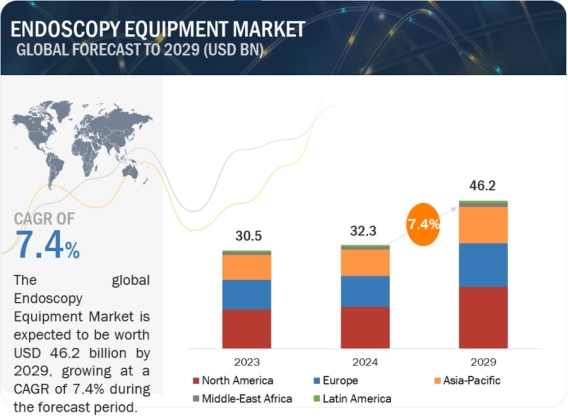

Insightful Endoscopy Equipment: Market Trends and Opportunities https://www.marketsandmarkets.com/Market-Reports/endoscopy-devices-market-689.html The global endoscopy equipment market is projected to reach USD 46.2 billion by 2029 from USD 32.3 billion in 2024, at a CAGR of 7.4%. Endoscopy is a minimally-invasive method that uses specialised equipment to observe interior organs or tissues. These operations use a variety of tools, including scopes designed for specific procedures, anaesthetic apparatus, video screens, lighting devices, imaging technology, monitoring equipment, storage cabinets, video processors, insufflators, and carts. They are used by medical specialists such as gastroenterologists, cardiologists, nephrologists, neurologists, hepatologists, and gynaecologists to perform safe examinations and interventions. The prominent players of global endoscopy equipment market are Olympus Corporation (Japan), KARL STORZ SE & Co. KG (Germany), Boston Scientific Corporation (US), JOHNSON & JOHNSON (US), Stryker Corporation (US), Medtronic, plc (Ireland), Fujifilm Holdings Corporation (Japan), HOYA Corporation (Japan), Nipro Corporation (Japan), Smith & Nephew plc (UK), Intuitive Surgical, Inc. (US), Richard Wolf GmbH (Germany), Cook Medical (US), B. Braun Melsungen AG (Germany), ConMed Corporation (US), Ambu A/S (Denmark), CapsoVision, Inc. (US), Fortimedix Surgical B.V. (Netherlands), The Cooper Companies, Inc. (US), Laborie Medical Technologies Inc. (Canada), Teleflex Incorporated (US), Carl Zeiss AG (Germany), Dantschke Medizintechnik GMBH & Co. KG (Germany), and Arthrex, Inc. (US)). These companies adopted strategies such as product launches, partnerships, acquisitions, and expansions to strengthen their presence in the endoscopy equipment market.

Insightful Endoscopy Equipment: Market Trends and Opportunities https://www.marketsandmarkets.com/Market-Reports/endoscopy-devices-market-689.html The global endoscopy equipment market is projected to reach USD 46.2 billion by 2029 from USD 32.3 billion in 2024, at a CAGR of 7.4%. Endoscopy is a minimally-invasive method that uses specialised equipment to observe interior organs or tissues. These operations use a variety of tools, including scopes designed for specific procedures, anaesthetic apparatus, video screens, lighting devices, imaging technology, monitoring equipment, storage cabinets, video processors, insufflators, and carts. They are used by medical specialists such as gastroenterologists, cardiologists, nephrologists, neurologists, hepatologists, and gynaecologists to perform safe examinations and interventions. The prominent players of global endoscopy equipment market are Olympus Corporation (Japan), KARL STORZ SE & Co. KG (Germany), Boston Scientific Corporation (US), JOHNSON & JOHNSON (US), Stryker Corporation (US), Medtronic, plc (Ireland), Fujifilm Holdings Corporation (Japan), HOYA Corporation (Japan), Nipro Corporation (Japan), Smith & Nephew plc (UK), Intuitive Surgical, Inc. (US), Richard Wolf GmbH (Germany), Cook Medical (US), B. Braun Melsungen AG (Germany), ConMed Corporation (US), Ambu A/S (Denmark), CapsoVision, Inc. (US), Fortimedix Surgical B.V. (Netherlands), The Cooper Companies, Inc. (US), Laborie Medical Technologies Inc. (Canada), Teleflex Incorporated (US), Carl Zeiss AG (Germany), Dantschke Medizintechnik GMBH & Co. KG (Germany), and Arthrex, Inc. (US)). These companies adopted strategies such as product launches, partnerships, acquisitions, and expansions to strengthen their presence in the endoscopy equipment market. -

-

Revolutionizing Healthcare: The Rise of Home Healthcare Market https://www.marketsandmarkets.com/Market-Reports/home-healthcare-equipment-market-696.html The global home healthcare market is projected to reach USD 383.0 Billion by 2028 from USD 250.0 Billion in 2023, at a CAGR of 8.9% during the forecast period Growth in this market is primarily driven by expansial growth in the old age population, and the rising incidence of chronic diseases. The key players operating in home healthcare market include Fresenius SE & Co. KGaA (Germany), Abbott (US), GE HealthCare (US), Koninklijke Philips N.V. (Netherlands), ResMed, Inc. (US), Linde plc (Ireland), F. Hoffman-La Roche, Ltd. (Switzerland), A&D Company, Limited (Japan), Bayada Home Health Care (US), Invacare Corporation (US), Amedisys (US), LHC Group, Inc. (US), OMRON Corporation (Japan), Drive DeVilbiss Healthcare (UK), Sunrise Medical (Germany), Roma Medical (UK), CAREMAX Rehabilitation Equipment Co., Ltd. (China), Vitalograph (UK), Advita Pflegedienst GmbH (Germany), RENAFAN GmbH (Germany), CONTEC MEDICAL SYSTEMS Co., Ltd. (China), B. Braun Melsungen Ag (Germany), Baxter International, Inc. (US), Medline Industries, Inc. (US), and Advin Health Care (India).

Revolutionizing Healthcare: The Rise of Home Healthcare Market https://www.marketsandmarkets.com/Market-Reports/home-healthcare-equipment-market-696.html The global home healthcare market is projected to reach USD 383.0 Billion by 2028 from USD 250.0 Billion in 2023, at a CAGR of 8.9% during the forecast period Growth in this market is primarily driven by expansial growth in the old age population, and the rising incidence of chronic diseases. The key players operating in home healthcare market include Fresenius SE & Co. KGaA (Germany), Abbott (US), GE HealthCare (US), Koninklijke Philips N.V. (Netherlands), ResMed, Inc. (US), Linde plc (Ireland), F. Hoffman-La Roche, Ltd. (Switzerland), A&D Company, Limited (Japan), Bayada Home Health Care (US), Invacare Corporation (US), Amedisys (US), LHC Group, Inc. (US), OMRON Corporation (Japan), Drive DeVilbiss Healthcare (UK), Sunrise Medical (Germany), Roma Medical (UK), CAREMAX Rehabilitation Equipment Co., Ltd. (China), Vitalograph (UK), Advita Pflegedienst GmbH (Germany), RENAFAN GmbH (Germany), CONTEC MEDICAL SYSTEMS Co., Ltd. (China), B. Braun Melsungen Ag (Germany), Baxter International, Inc. (US), Medline Industries, Inc. (US), and Advin Health Care (India). -

-

Battle for Glory: Spain vs. England FIFA Women's World Cup Final! Spain vs England FIFA Womens World Cup Final Visit- https://www.icecric.news/spain-vs-england-fifa-womens-world-cup-final/ #England #FIFAWomensWorldCup #FIFAWomensWorldCupFinal #Spain #SpainvsEnglandFIFAWomensWorldCupFinal #Gambhir #BabarAzam #Naseem #FormerWWE #Giannis #WillSmith #Braun #Football #Sports #IceCricNews

-

-

Shaping the Future of Healthcare: An In-depth Analysis of the Medical Electrodes Market https://www.marketsandmarkets.com/Market-Reports/medical-electrode-market-171260948.html The global medical electrode market is projected to reach USD 2.1 billion by 2026 from USD 1.7 billion in 2021, at a CAGR of 4.3% during the forecast period. Market growth is largely driven by rising incidence of neurological & cardiovascular disorders, increasing investments in research for medical devices, and growing preference for home & ambulatory care services. Emerging markets in developing economies are expected to offer potential growth opportunities for players operating in the market. The medical electrodes market is segmented based on product, technology, usability, application, and region The global medical electrodes market is fragmented. The prominent players operating in this market include Medtronic (Ireland), Ambu A/S (Denmark), 3M (US), Natus Medical Incorporated (US), Koninklijke Philips N.V. (Netherlands), B. Braun Melsungen AG (Germany), ZOLL Medical Corporation (US), Cardinal Health (US), CONMED Corporation (US), Nihon Kohden Corporation (Japan), Rhythmlink International, LLC (US), Cognionics, Inc. (US), GE Healthcare (US), Compumedics Limited (Australia), and Nissha Medical Technologies (Japan).

Shaping the Future of Healthcare: An In-depth Analysis of the Medical Electrodes Market https://www.marketsandmarkets.com/Market-Reports/medical-electrode-market-171260948.html The global medical electrode market is projected to reach USD 2.1 billion by 2026 from USD 1.7 billion in 2021, at a CAGR of 4.3% during the forecast period. Market growth is largely driven by rising incidence of neurological & cardiovascular disorders, increasing investments in research for medical devices, and growing preference for home & ambulatory care services. Emerging markets in developing economies are expected to offer potential growth opportunities for players operating in the market. The medical electrodes market is segmented based on product, technology, usability, application, and region The global medical electrodes market is fragmented. The prominent players operating in this market include Medtronic (Ireland), Ambu A/S (Denmark), 3M (US), Natus Medical Incorporated (US), Koninklijke Philips N.V. (Netherlands), B. Braun Melsungen AG (Germany), ZOLL Medical Corporation (US), Cardinal Health (US), CONMED Corporation (US), Nihon Kohden Corporation (Japan), Rhythmlink International, LLC (US), Cognionics, Inc. (US), GE Healthcare (US), Compumedics Limited (Australia), and Nissha Medical Technologies (Japan). -

-

Caring for Patients at Home: A Growing Trend in the Healthcare Industry https://www.marketsandmarkets.com/Market-Reports/home-healthcare-equipment-market-696.html The global home healthcare market is projected to reach USD 340.2 billion by 2027 from USD 226.0 billion in 2022, at a CAGR of 8.5% during the forecast period Growth in this market is mainly driven by rapid growth in the elderly population, and the rising incidence of chronic diseases. The key players in this market are Fresenius SE & Co. KGaA (Germany), Linde, Plc (Ireland), F.Hoffmann-La Roche, Ltd. (Switzerland), A&D Company, Limited (Japan), Bayada Home Health Care (US), Invacare Corporation (US), Abbott (US), Amedisys (US), ResMed, Inc. (US), LHC Group, Inc. (US), Omron Corporation (Japan), Koninkluke Philips N.V. (Netherlands), GE Healthcare (US), Drive Devilbiss Healthcare (UK), Hamilton Medical (Switzerland), Sunrise Medical (Germany), Roma Medical (UK), Caremax Rehabilitation Equipment Co., Ltd. (China), Vitalograph (UK), Advita Pflegedienst Gmbh (Germany), Renafan Gmbh (Germany), ADMR (France), Apex Medical Corp. (Taiwan), Contec Medical Systems Co., Ltd. (China), Löwenstein Medical Technology Gmbh + Co., KG. (Germany), B. Braun Melsungen Ag (Germany), Baxter International, Inc. (US), Allied Healthcare Products, Inc. (US), Medline Industries, Inc. (US), and Advin Health Care (India).

Caring for Patients at Home: A Growing Trend in the Healthcare Industry https://www.marketsandmarkets.com/Market-Reports/home-healthcare-equipment-market-696.html The global home healthcare market is projected to reach USD 340.2 billion by 2027 from USD 226.0 billion in 2022, at a CAGR of 8.5% during the forecast period Growth in this market is mainly driven by rapid growth in the elderly population, and the rising incidence of chronic diseases. The key players in this market are Fresenius SE & Co. KGaA (Germany), Linde, Plc (Ireland), F.Hoffmann-La Roche, Ltd. (Switzerland), A&D Company, Limited (Japan), Bayada Home Health Care (US), Invacare Corporation (US), Abbott (US), Amedisys (US), ResMed, Inc. (US), LHC Group, Inc. (US), Omron Corporation (Japan), Koninkluke Philips N.V. (Netherlands), GE Healthcare (US), Drive Devilbiss Healthcare (UK), Hamilton Medical (Switzerland), Sunrise Medical (Germany), Roma Medical (UK), Caremax Rehabilitation Equipment Co., Ltd. (China), Vitalograph (UK), Advita Pflegedienst Gmbh (Germany), Renafan Gmbh (Germany), ADMR (France), Apex Medical Corp. (Taiwan), Contec Medical Systems Co., Ltd. (China), Löwenstein Medical Technology Gmbh + Co., KG. (Germany), B. Braun Melsungen Ag (Germany), Baxter International, Inc. (US), Allied Healthcare Products, Inc. (US), Medline Industries, Inc. (US), and Advin Health Care (India).

Copyright 2019 © P-tweets Refunds